Learn about impairment of assets according to IAS 36, ensuring assets are valued correctly. Explore identifying impairment, sources of information, and an example of impairment considerations.

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

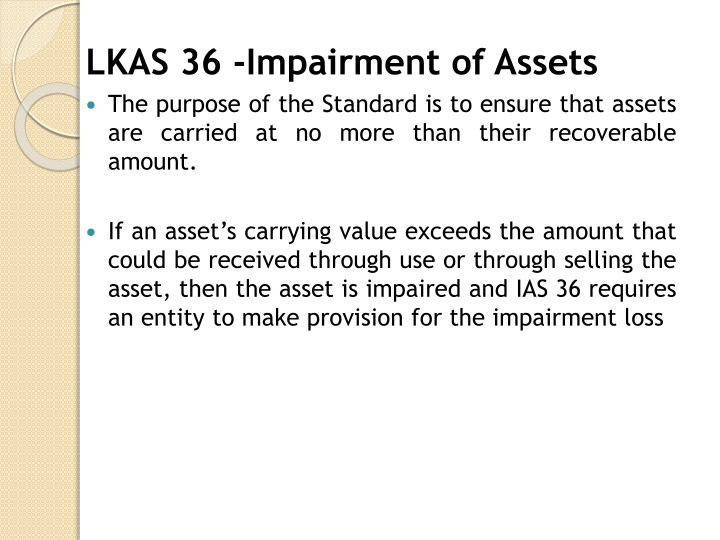

LKAS 36 -Impairment of Assets The purpose of the Standard is to ensure that assets are carried at no more than their recoverable amount. If an asset s carrying value exceeds the amount that could be received through use or through selling the asset, then the asset is impaired and IAS 36 requires an entity to make provision for the impairment loss

Identifying an Impairment loss An entity has to assess at the end of each reporting period whether there is any indication that an asset is impaired. Further, even if there is no indication of any impairment, these assets should be tested for impairment. An intangible asset that has an indefinite useful life An intangible asset that is not yet available for use Goodwill that has been acquired in a business combination

Ex: Impairment Considerations Machinery was originally acquired for LKR 80,000. It was expected to have a useful life of ten years and no residual value. At the start of year six, there was a downturn in demand due to a competitor product entering the market, and this has led to an impairment of the asset. The impairment has been calculated as being LKR20,000, although it is expected that the asset will continue to have a remaining five-year life. At the end of year five, the asset had a carrying amount of LKR 40,000 (LKR80,000 5/10 years). The impairment reduces the carrying amount of the asset to LKR 20,000 (LKR 40,000 less LKR 20,000) which should be depreciated over the remaining life of five years.