Central Sales Tax and Its Implications

Central Sales Tax is an indirect tax imposed on inter-state sales by the Central government but collected by the state government where the goods are sold. This tax is applicable only on inter-state trade and not on sales within a state. Learn more about the definition and scope of sales under Central Sales Tax Act.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

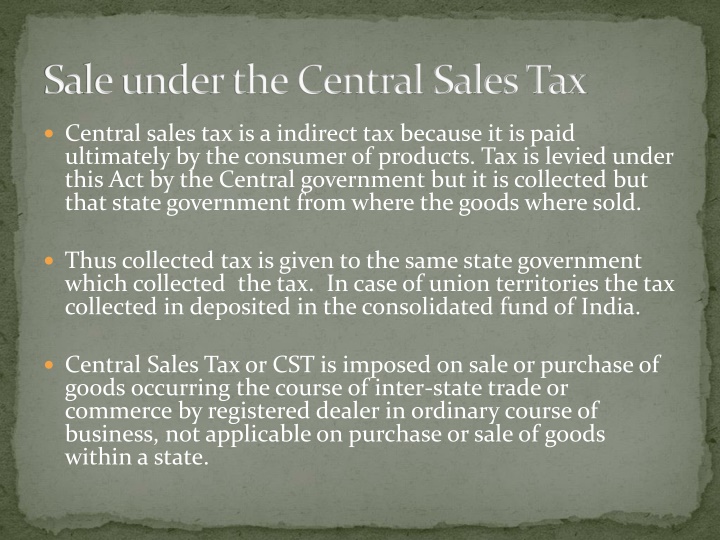

Sale under the Central Sales Tax Central sales tax is a indirect tax because it is paid ultimately by the consumer of products. Tax is levied under this Act by the Central government but it is collected but that state government from where the goods where sold. Thus collected tax is given to the same state government which collected the tax. In case of union territories the tax collected in deposited in the consolidated fund of India. Central Sales Tax or CST is imposed on sale or purchase of goods occurring the course of inter-state trade or commerce by registered dealer in ordinary course of business, not applicable on purchase or sale of goods within a state.

To be continue.. Therefore, it is more important to know that, what is sale under Central Sale Tax? In other words CST is applicable only in the case of inter-state sales and not on sales made within the state or import/export of sales . For the better understanding of Inter-state sale, in general sense is when a sale or purchase constitutes movement of goods from one state to another. Accordingly, a consignment to agents or transfers of goods to branch or other offices is not a sale as per the CST Act.

Definition of sale under CST Definition- Under section 2(g) - sale , with its grammatical variations and cognate expressions, means any transfer of property in goods by one person to another for cash or deferred payment or for any other valuable Consideration, and includes, A transfer, otherwise than in pursuance of a contract, of property in any goods for cash, deferred payment or other valuable consideration; A transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract; 1. 2.

To be continue.. 3. A delivery of goods on hire-purchase or any system of payment by installments; A transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration; A supply of goods by any unincorporated association or body of persons to a member thereof for cash, deferred payment or other valuable consideration; A supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (whether or not intoxicating), where such supply or service, is for cash, deferred payment or other valuable consideration, But does not include a mortgage or hypothecation of or a charge or pledge on goods. 4. 5. 6.

Ingredients of sale According to definition of sale there are some important ingredients of its: Two persons 1) Transfer of property in goods by one person to another 2) For cash or differed payment or any other valuable consideration. 3) There are six type of deemed sales also included in the definition of sale Transfer of property other than sale a) Hire purchase at the time of delivery of goods b) Goods involved in works contract c) Transfer of right to use goods d) Supply by clubs and Association to its members e) Supply of foods and beverages along with services f) Proviso- But does not include a mortgage or hypothecation of or a charge or pledge on goods.