COMPETITION IN DIGITAL FINANCIAL SERVICES IN BANGLADESH

Bangladesh has a growing landscape in mobile uses and mobile financial services, with high mobile penetration levels especially in rural areas. The country's demographic characteristics show a significant rural-urban divide, with a large working-age population and varying access to electricity and financial institutions. The financial system of Bangladesh includes a mix of state-owned, specialized, private commercial, and foreign banks, along with a network of ATMs and non-bank financial institutions. The digital financial services infrastructure in Bangladesh is advancing rapidly through initiatives in both traditional banking and mobile financial services, supported by robust technology infrastructure.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

COMPETITION IN DIGITAL FINANCIAL SERVICES IN BANGLADESH Mohammad Naushad Ali Chowdhury Executive Director Bangladesh Bank

MOBILE USES AND MFS LANDSCAPE IN BANGLADESH Bangladesh is one of the most populous and most densely populated countries in the world. Mobile penetration levels are relatively high, even in rural areas (something not seen in most other emerging markets). Mobile operators has immense scope to develop new revenue streams beyond core mobile connectivity services that support basic human needs around agriculture, education, employment. The use of mobile in improvement is on the rise. MFS growth for the last few years were phenomenal. businesses and driving socio-economic

MOBILE USES AND MFS LANDSCAPE IN BANGLADESH The country now has a relatively solid mobile consumer base, much of which still have immense potential for serving core life needs like mobile money and its ancillary and related services. Bangladesh Bank the mobile money regulator in the country sees the existing bank led model suitable for the country while being open to new investment in innovation and technology Mobile operators are demonstrating the potential for social VAS, while MFS provider are coming up with various VAS in the mobile money landscape. We expect this to continue to grow, while we also understand it will take time. There is still an opportunity for public and private investment in providing seed capital for the innovation that is not yet market-led , with a key role for government in facilitating this process. Although we have introduced simplified CDD for MFS account but all activities are under AML/CFT regulation of Bangladesh Bank.

BANGLADESH DEMOGRAPHIC CHARACTERISTICS Rural Urban divide Rural Urban 88% 46% 43% 38% 35% 21% Age Structure----------65% working age population 65 + years 5 Poverty Head count ratio at national poverty incidence Access to Electricity Access at Formal Financial institutions 55-64 years 5.9 25-54 years 38 15-24 years 18.8 0-14 years 32.3

FINANCIAL SYSTEM OF BANGLADESH 4 State owned Commercial Banks 4 Specialized Banks 39 Private commercial Banks 9 Foreign Banks 9400 Branches country wide Schedul ed Banks 56 ATMs network- 6035 Non Bank Financial Institutions -33 Central Banks MFIs-697, MFIs branches- 18000 4 Non Schedul ed Banks

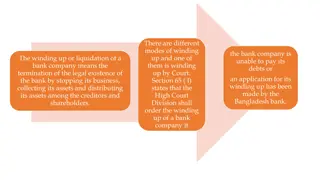

DIGITAL FINANCIAL SERVICES INFRASTRUCTURE Digital Initiatives are in two fronts In the Banking through introduction of internet, SMS, ATMs, POS based transaction Through MFS by the mobile bank account /mobile wallet BB has built a robust technology infrastructure with various enablement's to support digital financial services: Online Credit & Supervisory reporting Electronic Fund transfer Bangladesh Automated clearing house National Payment Switch Real-time Gross Settlement systems Bangladesh Bank in association with the NID authority further wants to connect NID with the digital banking and MFS system to introduce e-KYC. Following initiatives are underway : NID linked G2P payments Union Digital Centers Agent Banking; POS, rural branches, Rural Savings Bank

MFS CURRENTSTATUS Digital Financial Services (DFS) in Bangladesh (As on October 2015) Banking End Number of POS Number of ATMs Number of bank branches Agents (Banking)- MFS providers Licensed Providers Active Providers- ATMs- Agents- MFS transaction snapshot Average Daily Transaction (Value million USD)- Active Customers number (million) Average Daily Transactions (million Number) 28265 6311 9500 148 28 20 3905 547813 55.73 12.06 3.58 Key MFS indicators Number of Agents (million) Number of Registered clients (million) Number of Transaction (million) Value of Transaction (million USD) Jun 2013 0.10 6.67 17.6 539.23 Dec 2013 0.189 13.18 31.36 852.62 Dec 2014 0.541 25.2 74.47 1343.98 Jun 2015 0.538 28.65 96.16 1662.76 Sep 2015 0.542 29.21 106.43 1931.51

ISSUESAROUNDCOMPETITIONIN DFS SPACE Investment USSD price Pricing Innovation for mass use Product development and value proposition OTC Market opening for non-bank entities