Learn about consignment accounting, where goods are sent by a consignor to a consignee for sale while maintaining ownership. Explore the features, important terms, accounting treatment, journal entries, and profit/loss calculation in consignment accounting.

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

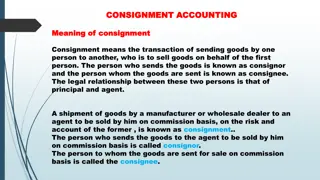

Introduction to Consignment Consignment is a business arrangement where goods are sent by one party (Consignor) to another (Consignee) for sale. Ownership remains with the Consignor until goods are sold. The Consignee earns a commission for selling the goods.

Features of Consignment Ownership remains with the Consignor. The Consignee does not own the goods but sells them on behalf of the Consignor. Profit or loss belongs to the Consignor. The Consignee earns a commission on sales.

Important Terms in Consignment Consignor: The person who sends goods for sale. Consignee: The agent who sells the goods. Proforma Invoice: Document sent with goods detailing quantity and expected price. Del Credere Commission: Extra commission for taking responsibility for bad debts.

Accounting Treatment in Consignment 1. Recording of Goods Sent on Consignment 2. Recording of Expenses Incurred 3. Recording of Sales & Commission 4. Recording of Unsold Stock 5. Calculation of Profit or Loss on Consignment

Journal Entries for Consignment For Goods Sent on Consignment: Dr. Consignment A/c Cr. Goods Sent on Consignment A/c For Expenses Paid by Consignor: Dr. Consignment A/c Cr. Cash/Bank A/c For Sales by Consignee: Dr. Bank A/c Cr. Consignee A/c For Commission Payable: Dr. Consignment A/c Cr. Consignee A/c For Closing Stock: Dr. Closing Stock A/c Cr. Consignment A/c

Calculation of Profit/Loss on Consignment Profit/Loss = Sales - (Cost of Goods + Expenses + Commission) If positive, it's a Profit. If negative, it's a Loss.

Practical Example 100 units sent at 500 each. Expenses: 5,000 (Freight, Insurance). 80 units sold at 700 each. Commission @5% on sales. Calculate profit/loss.

Conclusion Consignment helps businesses expand without opening branches. Proper accounting ensures accurate calculation of profit/loss. Understanding journal entries is crucial for financial transparency.