Impact of Income Tax Exemptions on Educational Institutions

Explore the intricacies of income tax exemptions for educational institutions under Section 10(23C) and Section 10(23C)(iiiad), including the criteria, limits, and implications. Learn about applicable TDS rates for various types of payments and the significance of PAN and TAN in tax compliance. Discover the due dates for TDS payments and gain insights into managing tax responsibilities effectively.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

MVC 4/8/2025 1

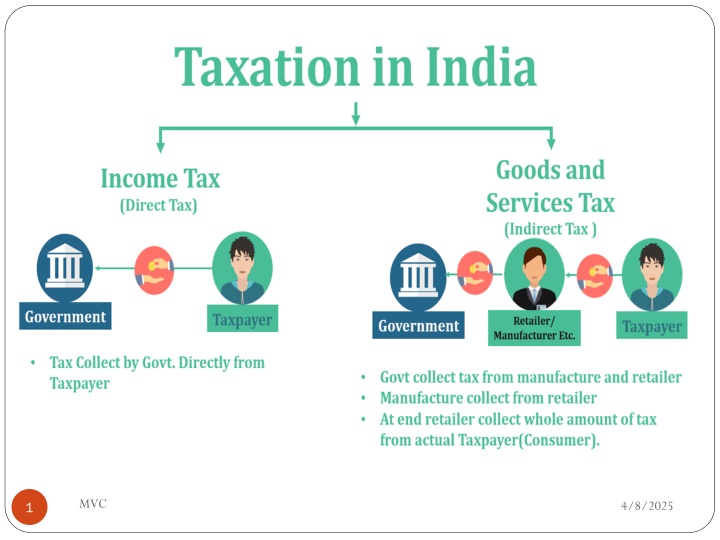

INCOME TAX & EDUCATIONAL INSTITUTION MVC 4/8/2025 2

INCOME GENERATED BY GOVT EDUCATIONAL INSTITUTION Income generated by any educational institute or any university solely for the purpose of education and not for profit-making and which is substantially or wholly financed by the government is fully exempted by the Income Tax under section 10(23C)(iiiab). Hence, it is clear that educational institution is fully exempted under the income tax until and unless it is not for profit purpose. Under section 10(23C) (iiiad) it is stated that the revenue earned by the university or any educational institution existing only for the educational purposes rather than the profit purpose shall be exempted from the income tax if the total yearly receipts of such educational institution or the university shall not exceed Rs. one crore. Exceeding Rs 1 crore :The educational institution must spend its income exclusively or wholly to the purpose and objects for what it were established. Moreover, the educational institution must apply at a minimum of 85% of his income every year. Hence, just the registration U/s 10(23C) by itself does not mean or result in the exemption. Further, it must be noted that the educational institution is allowed to retain up to 15% of the total income. In any case, when the institution is unable to maintain 85% of the income, the educational institution shall accumulate the excess income for application in the coming years but not exceeding five years. MVC 4/8/2025 3

APPLICABLE TDS RATES Payment of salary to a resident/non-resident -(Sec. 192) Normal Tax (SC : 15% on income exceeding Rs. 1cr. EC : 2%, SHEC : 1% ) Rate %(Maximum marginal rate in case PAN is not furnished by the recipient) Payment of accumulated balance due to an employee-(Sec. 192A) 10 Advertisement 1% Payment to resident contractor/sub-contractor - (Sec. 194C) a. 1% (individual)/ 2%(company) Rent to a resident (Sec. 194-I) a. Rent of plant and machinery 2% b. Rent of land or building or land appurtenant to a building or furniture or fittings 10% (However, amount upto Rs. 1,80,000/- is not liable for TDS) Fees for professional or technical services to a resident (Sec. 194J) 10 %(However, amount upto Rs. 30,000/- is not liable for TDS) MVC 4/8/2025 4

PAN & TAN A PAN is a permanent account number which is a ten-character alphanumeric identifier, issued in the form of a laminated "PAN card", by the Indian Income Tax Department, to any "person" who applies for it or to whom the department allots the number without an application. TAN:Tax Deduction Account Number or Tax Collection Account Number is a 10 - digit alpha-numeric number issued by the Income-tax Department. TAN is to be obtained by all persons who are responsible for deducting tax at source (TDS) or who are required to collect tax at source (TCS). MVC 4/8/2025 5

TDS DUE DATES The due dates for payment of TDS are the 7th of next month in which TDS is deducted/credited and for the month of March, it is 30th April. The due dates for return filing of TDS are the last date of the month after quarter-end, and for the last quarter, the due date is 31st May MVC 4/8/2025 6

TDS RETURNS 1st Quarter 1st April to 30th June .31st July 2022 2nd Quarter 1st July to 30th September .31st October 2022 3rd Quarter 1st October to 31st December 31st Jan 2023 4th Quarter 1st January to 31st March 31st May 2023 MVC 4/8/2025 7

FORM 16/ FORM 16 A As per the provisions of the Income Tax Act, TDS certificate must be issued by employers to an employee within 15 days of filing their fourth-quarter TDS returns. Hence, Form 16 must be issued within 15 days of filing the fourth quarter TDS returns. Form 16A is issued quarterly. The due date is 15th of the month following the due date for quarterly TDS return MVC 4/8/2025 8

FORM 24 Q & 26 Q Forms 24Q, 26Q, 27Q, 27EQ, 27D are all income tax return forms to declare Tax Deducted at Source (TDS) and have to be submitted to the Income Tax Department. Each one has a different purpose but connected with income tax. Form 24Q:This form has to be filled up for declaration of a citizen s TDS returns in detail.The form information is based on a citizen s salary payments and the deductions made for tax. The declaration and payment is to be made quarterly by companies and firms in India. Form 26Q:This form has to be filled up for declaration of a citizen s TDS returns in detail. This form is based on their payments other than salary. Form 27D: This is a Certificate under section 206C of the Income tax Act, 1961 for tax that is collected at source. MVC 4/8/2025 9

TDS PENALTIES & INTEREST Particulars Minimum Penalty Maximum Penalty Late filing of Form 24Q (Penalty under Section 234E) Rs 200 per day until TDS return is filed Penalty amount should not exceed tax deducted Non- filing of Form 24Q (Penalty under Section 271H) Rs 10,000 Rs 1,00,000 Under Section 201(1A), in case off late deposit of TDS after deduction, you have to pay interest. Interest is calculated at the rate of 1.5% per month from the date on which TDS was deducted to the actual date of deposit MVC 4/8/2025 10

SALARY TAX SLABS Up to Rs. 2,50,000 Nil Rs. 2,50,001- Rs. 5,00,000 5% Rs. 5,00,001- Rs. 10,00,000 20% Above Rs. 10,00,000 30% Total Income (Rs) Rate Up to 2,50,000 Nil From 2,50,001 to 5,00,000 5% From 5,00,001 to 7,50,000 10% From 7,50,001 to 10,00,000 15% From 10,00,001 to 12,50,000 20% From 12,50,001 to 15,00,000 25% Above 15,00,000 30% MVC 4/8/2025 11

TAX SAVINGS/DEDUCTIONS 80 C RS 1.50 lacs 80 D Rs 0.25 lacs 80 CCD Rs0.50 lacs SEC 24 Rs 2.00 lacs 80 DDB Rs 1.00 lacs 80 G DONATION 80 TTA Rs 0.10 lacs 80 E INTEREST ON EDUCATION LOAN 80 U DISABLED MVC 4/8/2025 12

ONE NATION ONE TAX MVC 4/8/2025 13

GOODS & SERVICES TAX MVC 4/8/2025 14

WHY GST MVC 4/8/2025 15

GST REGISTRATION REQUIREMENTS MVC 4/8/2025 16

GSTN 15 DIGIT NUMBER PAN BASED MVC 4/8/2025 17

GST ON HIGHER EDUCATION Educational institutions up to Higher Secondary School level do not suffer GST on output services and also on most of the important input services. Some of the input services like canteen, repairs and maintenance etc. provided by private players to educational institutions were subject to service tax in pre-GST era and the same tax treatment has been continued in GST regime. Thus output services of lodging/boarding in hostels provided by such educational institutions which are providing pre-school education and education up to higher secondary school or equivalent or education leading to a qualification recognised by law, are fully exempt from GST. Annual subscription/fees charged as lodging/ boarding charges by such educational institutions from its students for hostel accommodation shall therefore, not attract GST. Similarly, output services related to the specified courses provided by IIM s would be exempt. Executive Development Programs run by the IIM s are specifically excluded, hence such courses would be subject to GST. MVC 4/8/2025 18

EDUCATIONAL SERVICES EXEMPT UNDER GST 1. Educational institution providing pre-school education and education up to higher secondary school or equivalent. (1) Transportation of students, faculty and staff; (2) Catering, including any mid-day meals scheme sponsored by the Central Government, State Government or Union territory; (3) Security or cleaning or house-keeping services performed in such educational institution; v Services relating to admission to, or conduct of examination by, such institution 2. Educational institution providing education as a part of a curriculum for obtaining a recognised qualification (1) Services relating to admission to, or conduct of examination by, such institution (2)Supply of online educational journals or periodical 3. Educational institution providing education as a part of approved vocational education course (1) Services relating to admission to, or conduct of examination by, such institution. MVC 4/8/2025 19

GST HSN CODE 9992 9992 Education Services 18% ( 9% Central Tax + 9% State Tax)/ Serial No. 30 of Notification No. 11/2017-Central Tax (Rate) dated 28th June, 2017 9992 Services provided (a) by an educational institution to its students, faculty and staff; (b) to an educational institution, by way of, - (i) Transportation of students, faculty and staff; (ii) Catering, including any mid-day meals scheme sponsored by the Central Government, State Government or Union territory; (iii) Security or cleaning or housekeeping services performed in such educational institution; (iv) Services relating to admission to, or conduct of examination by, such institution; up to higher secondary: (v) Provided that nothing contained in entry (b) shall apply to an educational institution other than an institution providing services by way of pre-school education and education up to higher secondary school or equivalent NIL / MVC 4/8/2025 20

NOTIFICATION 9992 SERVICES PROVIDED BY IIM As per the guidelines of the Central Government, to their students, by way of the following educational programmes, except Executive Development Programme: - (a) two year full time Post Graduate Programmes in Management for the Post Graduate Diploma in Management, to which admissions are made on the basis of Common Admission Test (CAT) conducted by the Indian Institute of Management; (b) fellow programme in Management; (c) five year integrated programme in Management. NIL / Serial No. 67 of Notification No. 12/2017- Central Tax (Rate) dated 28th June, 2017 90 or any chapter .NIL (c )Technical aids for education, rehabilitation, vocational training and employment of the blind such as Braille typewriters, braille watches, teaching and learning aids, games and other instruments and vocational aids specifically adapted for use of the blindBraille instruments, paper etc. 5%/ Serial No. 257 of Schedule I of the Notification No.1/2017-Central Tax (Rate) dated 28th June, 2017 9023 (d)Instruments, apparatus and models, designed for demonstrational purposes (for example, in education or exhibitions), unsuitable for other uses .28 %/ Serial No. 191 of Schedule IV of the Notification No.1/2017-Central Tax (Rate) dated 28th June, 2017 MVC 4/8/2025 21

SERVICES TAXABLE/EXEMPT 1) Renting of school bus to an education institution: Services provided by way of renting of school buses is liable to tax since the above entry covers transportation services only. In the instant case, it is of renting of motor vehicles. 2) Catering services provided to educational institution: If the educational institution outsources the catering activity to an outside contractor, then it is a supply of service to the concerned educational institution by such outside caterer. Catering services provided to an educational institution shall be exempted only if such services are provided to an educational institution providing pre-school education and education up to higher secondary school or equivalent. 3) Supply of fixed assets like sale of benches, projector, furniture etc., to an educational institution: Fixed assets supplied to an educational institution is taxable as the exemption entry is applicable only on services provided to an educational institution. 4) Advertisement services provided to an educational institution: Educational institution procures services from advertising agencies for promoting their brand or institution, such advertisement services shall be taxable as the same is not included in the exemption entry. MVC 4/8/2025 22

SERVICES TAXABLE/EXEMPT 5) Services like Karate, Music, Swimming provided directly to the students of educational institution: In terms of exemption entry services provided by an educational institution to its students is exempt, however the exemption shall not be applicable is the services are provided by a third-party service vendor directly to the students. If consideration for such services is paid by students to the educational institution which in turn is paid to the third-party services provider Even if consideration is routed through educational institution, it can be said that the service is provided directly to the students and not to the educational institution, As the definition of consideration includes payment made by any other person other than institution which means that consideration can be routed from third person. 6) Sale of Books, Uniform, Stationary to an educational institution: Sale of books, uniform and stationery to educational institution is taxable/exempt based on their classification (HSN). 7) Admission services to educational institution: Admission services that is services such as enrolling students is exempted. MVC 4/8/2025 23

SERVICE TAXABLE/EXEMPT 8) Lunch management services/Transport management services provided to an educational institution: Lunch management services such as food items to be included in menu, arranging food to the students, arranging plates/tables and transport management services such as arranging time slots for picking/dropping students, supply of drivers etc., is taxable as such services will not be covered under catering (As it does not involve supply of food) and transportation services (as vehicle is not rented by the supplier only management services are provided). 9) Campus placement services provided to educational institutions for securing job placements for the students Campus placement services provided to an educational institution are taxable as the same are not covered in the exemption entry. 10) Renting of building to an educational institution: Renting of building to an educational institution is taxable as rental services are not covered in the exemption entry. MVC 4/8/2025 24

ELIGIBILITY FOR INPUT TAX CREDIT Eligibility of Input tax credit to an Educational institution: 1) Education institution is not eligible to avail input tax credit on inputs/input services which are exclusively used for effecting exempt supplies. 2) However, such institutions are eligible to avail input tax credit on input/input services which are used for effecting taxable supplies. 3) On inputs/inputs services which are used for effecting both taxable and exempt supplies input tax credit eligible to b MVC 4/8/2025 25

REVERSE CHARGE MECHANISM OUTSOURCED SECURITY @ 18% LEASED VEHICLE @ 18% LEGAL SERVICES @ 18% MANPOWER OUTSOURCED @ 18% REPAIR & MAINTENANCE @ 18% MVC 4/8/2025 26

CONSTRUCTION AT COLLEGES GST IS PAYABLE ON LABOUR @ 18% GST IS PAYABLE ON COMPOSITE CONTRACTS AT 12% TDS WOULD BE DEDUCTIBLE ON TDS ON GST PAYMENTS MVC 4/8/2025 27

GST PAYMENT DUE DATES MVC 4/8/2025 28

GST DUE DATES FOR RETURNS MVC 4/8/2025 29

LATE FEES & INTEREST As per the GST laws, late fee is an amount charged for delay in filing the GST returns. A prescribed late fees will be charged for each day of delay, when a GST registered business misses filing GST returns within the prescribed due dates* The late fee should be paid in cash and the taxpayer cannot use the Input Tax Credit (ITC) available in electronic credit ledger for payment of late fee. The late fee is also applicable for the delay in filing nil returns. For example, one has to pay a late fee even though there are no sales or purchases and no GST liability to declare in the GSTR-3B. The late fee will depend upon the number of days of delay from the due date. GST return in GSTR-3B is filed on 23rd January 2021, 3 days after the prescribed due date i.e 20th January 2021. The late fees will be calculated for three days and it should be deposited in cash. However, currently, the GST portal is aligned to charge a late fee only on returns GSTR- 3B, GSTR-4, GSTR-5, GSTR-5A, GSTR-6, GSTR-8, GSTR-7 and GSTR-9 only. MVC 4/8/2025 30

QUANTUM OF LATE FEES In case of nil GSTR-1 and GSTR-3B filing, the maximum late fee charged shall be capped at Rs.500 per return (i.e Rs. 250 each for CGST & SGST). In GSTR-1 and GSTR-3B other than nil filing, maximum late fee is fixed based on annual turnover slab, as follows: If the annual turnover in the previous financial year is upto Rs.1.5 crore then the late fee of maximum Rs 2,000 per return can only be charged (i.e Rs.1000 each for CGST and SGST). If the turnover ranges between Rs.1.5 crore and Rs.5 crore then the maximum late fee of Rs.5,000 per return can only be charged (i.e Rs. 2500 each for CGST and SGST). If the turnover is more than Rs.5 crore then late fee of maximum Rs.10,000 (i.e Rs. 5000 per CGST and SGST) can be charged. Additionally, the late fee has been rationalised for delayed filing of GSTR-4 from FY 2021-22, via the CGST notification 21/2021 dated 1st June 2021. The maximum late fee will be restricted to Rs.500 per return for nil filing and Rs. 2000 for other than nil filing. According to CGST notification 22/2021 dated 1st June 2021, the late fee chargeable for GSTR-7 i.e TDS filing under GST shall be of maximum Rs. 2,000 while late fee per day charged is reduced from Rs.200 to Rs.50 per day of delay, per act, per return. MVC 4/8/2025 31