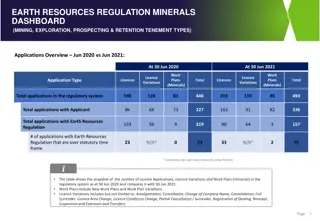

Impending Discount to Liquid NAV & Upside Potential Value by Altius Minerals

Altius Minerals presents an enticing investment opportunity with a discount to liquid NAV, significant upside potential, and a strong capital structure. Through royalty acquisition and investment, the company operates a capex-lite business model with stable finances and diverse mineral exploration projects. Enjoy downside protection, complementary businesses, and a lucrative Voiseys Bay Royalty. Explore Altius Minerals for a unique investment experience in the mining industry.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

An impending discount to liquid NAV + big upside potential ValueX June 21, 2013 Vail, Colorado

Altius Minerals Pay <$1 for $1 liquid NAV No credit for two developing royalties Pay nothing for massive upside potential $2.5 mm in after tax royalty payments in 2013 $2.5mm - $3 mm/year at current prices G&A $2mm-$3mm/year Stable share count, no debt

Two complimentary businesses Mineral exploration project generation & royalty creation Eastern Canada, Chile Royalty acquisition & investment The best business is a royalty on the growth of others requiring little capital itself. ~Warren Buffett, 1978 Berkshire annual report

Capex lite business model 56 partner funded projects since inception Partner exploration funding $150 million vs. $15 million from ALS Current NAV = $255mm I never want to be in the mining business. ~Brian Dalton, founder/CEO Altius Minerals

When it works Mineral & project location proceeds to ALS Partner ALS cost Royalty Uranium - Central Labrador Aurora Energy $650,000 $210 million 2% GSR Copper/gold - central Newfoundland (Ming Mine) Rambler Metals $600,000 $6 million n/a Iron ore in western Labrador (Kami project) Alderon Iron Ore $2 million $31 million 3% GSR

Downside protection $150 mm cash/treasurys ($5.33/share) $110 mm securities ($3.90) $8.4 mm Voisey s Bay Royalty ($0.30) $2-3mm/year royalties at $6 lb. nickel $12.9 mm total liabilities ($0.45) $9/share of decent NAV

Voiseys Bay Royalty Altius owns an effective 0.3% NSR on Voisey s Bay nickel Paid $13.6 million in 2003 Assumed $3.25/lb. nickel ($4 in 2009, $6+ now) Cumulative revenues ~$25 mm Est. mine life ~2036 Royalty covers all future expansion/development at zero extra cost Cash flow covers Altius G&A

Capital structure 28,854,364 fully diluted shares NCIB 1,406,207 Started 4/2/2013 Expires 4/1/2014 Automatic share repurchase plan 7,036 shares/day (NCIB 200 days) Zero debt Not your average geologist paycheck scheme

Upside potential: Kami project Altius discovered a 1 billion tonne resource in western Labrador Four producing mines, skilled labor, mining friendly jurisdiction, rail, deep sea ports, roads Created Alderon Iron Ore (ADV.TO) Altius owns 32.9 mm shares of ADV Alderon owns 75% of Kami LP Hebei Iron & Steel Group owns 20% of ADV.TO; 25% of Kami LP Hebei will offtake 60% of first 8 million tonnes Hebei paid $182 mm of $400mm committments

Upside potential: Kami Project Dec. 2012 feasibility study $1.3B capital cost to build the mine Kami mine = $2.46B NPV10 Altius owns 25% of 75% of that ~$461mm, or $16 Altius share, or 160% upside

Higher pricesbut no shortage Bloomberg News, June 20 Hebei Says Iron Ore to Recover to $140 on Higher Chinese Output We can see there will be no shortages Iron- ore prices are not going to go crazy high. ~Tian Zejun, president of Hebei s international trading unit

Kami royalty income projection Kami royalty Production commences Q4 2015 $27mm/year @ 8mmtpa FE 62% $54mm/year @ 16mmtpa FE 62% Mgmt stated intention is to dividend royalty income from Kami After royalty tax, maybe $0.76 - $1.52/share But, if I know Brian Dalton

Kami is farthest along 20 total projects right now 10 w/partners Project Partner Royalty Kami Western Labrador Labrador West iron ore Revelation Alaska Cristo Cu/Au Alaska Topsails Cu/Moly central NL Viking gold west NL CMB uranium central Labrador Humble Cu/Au Central Labrador Saglek - iron ore North Labrador Alderon Iron Ore Rio Tinto Millrock Millrock/Brixton JNR Resources Northern Abitibi Paladin Energy Millrock/Kinross Cliffs Natural Resources 3% GSR 3% GSR 2% NSR gold; 1% NSR base metals 2% NSR gold; 1% NSR base metals 2% GSR uranium/ 2% NSR other 2-4% sliding scale NSR 3% GSR 2% NSR gold; 1% NSR base metals 1% NSR

Wait til it trades below NAV, then buy it then wait some more. Thank you. dferris@stansberryresearch.com