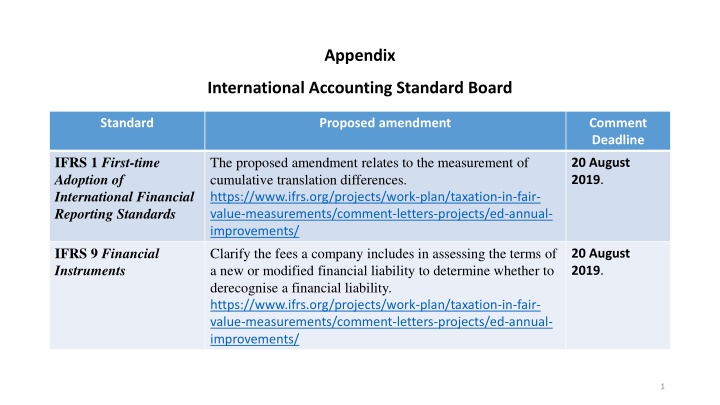

International Accounting Standard Board

This proposed amendment by the International Accounting Standards Board (IASB) concerns the measurement of cumulative translation differences in the context of IFRS 1 - First-time Adoption of International Financial Reporting Standards.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

Appendix International Accounting Standard Board Standard Proposed amendment Comment Deadline IFRS 1 First-time Adoption of International Financial Reporting Standards The proposed amendment relates to the measurement of cumulative translation differences. https://www.ifrs.org/projects/work-plan/taxation-in-fair- value-measurements/comment-letters-projects/ed-annual- improvements/ Clarify the fees a company includes in assessing the terms of a new or modified financial liability to determine whether to derecognise a financial liability. https://www.ifrs.org/projects/work-plan/taxation-in-fair- value-measurements/comment-letters-projects/ed-annual- improvements/ 20 August 2019. IFRS 9 Financial Instruments 20 August 2019. 1

Standard Proposed amendment Comment Deadline Illustrative Examples accompanying IFRS 16 Leases Remove the potential for confusion regarding lease incentives by amending an Illustrative Example accompanying IFRS 16. https://www.ifrs.org/projects/work-plan/taxation-in-fair- value-measurements/comment-letters-projects/ed-annual- improvements/ Align the fair value measurement requirements in IAS 41 with those in other IFRS Standards. https://www.ifrs.org/projects/work-plan/taxation-in-fair- value-measurements/comment-letters-projects/ed-annual- improvements/ 20 August 2019. IAS 41 Agriculture 20 August 2019. 2

Standard Proposed amendment Comment Deadline IFRS 17 Insurance contract 1. Scope exclusions credit cards and loans that meet the definition of an insurance contract 2. Expected recovery of insurance acquisition cash flows 3. Contractual service margin attributable to investment- return service and investment-related service 4. Reinsurance contracts held recovery of losses on underlying insurance contracts 5. Presentation in the statement of financial position 6. Applicability of the risk mitigation option 7. Effective date of IFRS 17 and the IFRS 9 Financial Instruments temporary exemption 8. Transition modifications and reliefs https://www.ifrs.org/projects/work-plan/amendments-to- ifrs-17/comment-letters-projects/ed-amendments-to-ifrs- 17/ 25 September 2019. 3

Standard Proposed amendment Comment Deadline IFRS 3 Business Combinations Updating the reference without making any other changes to IFRS 3 could change the accounting requirements for business combinations because the liability definition in the 2018 Conceptual Framework is broader than that in previous versions https://www.ifrs.org/projects/work-plan/updating-a- reference-to-the-conceptual-framework-ifrs-3/comment- letters-projects/ed-reference-to-the-conceptual-framework/ 27 September 2019 4