International Tax Law and Transfer Pricing: History and Interpretation

Explore the evolution of tax treaties, international tax determination, and the sources of international tax law. Learn about the significance of transfer pricing and how domestic statutes shape international tax principles.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

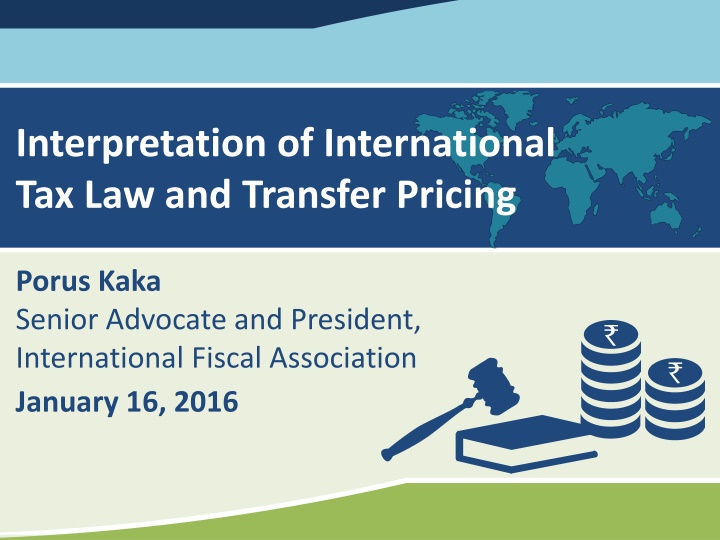

Interpretation of International Tax Law and Transfer Pricing Porus Kaka Senior Advocate and President, International Fiscal Association January 16, 2016 0

History of Tax Treaty (1/2) Earliest Treaty was adopted by Prussia around the start of the Twentieth Century First Treaty was with Austria signed in 1899 In 1920 League of Nations began to play a leadership role 1928 published the first internationally important Model Tax Conventions After World War I, Germany signed a treaty with Czechoslovakia in 1921 and with Austria in 1922 The League of Nations began publication on tax treaties in 1923 The OCED becomes the Organization for Economic Cooperation and Development 1

History of Tax Treaty (2/2) OCED first draft model treaty in 1963 United Nation published a manual for the negotiations of Bilateral Tax Treaties between developed and developing countries in 1979 In 1980 United Nations published a manual for the negotiations of Bilateral Tax Treaties between developed and developing countries OCED made some amendments published in loose lease form in 1990 s UN Model Tax Convention 2001 OCED started amending the publication every 2 to 3 years New UN Model on Tax Convention 2011 2

International Tax Determination of tax on an individual or entity, subject to laws in different jurisdictions Tax systems vary from country to country Taxation systems can be classified on the basis of Residency Territory Citizenship Issues faced in global tax scenario Double Taxation Fiscal Evasion Transfer Pricing Tax Avoidance Double non taxation Tax competition by states 3

Sources of International Tax Law Domestic Statutes Tax Treaties and Model Commentaries Circulars Judgments & Precedents 4

Domestic Statute Law Principle sections within the Income Tax Act, 1961 in which the basic principles of international tax law are enshrined under S.5. Scope of income S.9. Income deemed to be accrued or arise in India S.90. Double Taxation Relief; power to enter into treaties S.92. Computation of income from financial transactions having regard to arm s length price, commonly referred to as Transfer Pricing. 5

What is a tax treaty? Contract between countries governing issues of allocation of taxing rights on the basis of residence and/or source Undertaken with a view to grant relief for Avoidance of double taxation Prevention of fiscal evasion Promotion of mutual economic relations, trade and investment. Facilitates exchange of information and mutual agreements among Contracting States 6

Object of Tax Treaties Treaties cannot levy tax but can give relief- Azadi Bacho Andolan 263 ITR 706 (Sc) The Andhra Pradesh High Court in Sanofi s 354 ITR 316 (AP) made some key observations about the importance of DTAA s and their relevance in the global scenario In recognition of the pejorative effect of double taxation on exchange of goods and services and movement of capital, technology and persons, agreements/treaties/conventions/ protocols were entered into for removing obstacles that double-taxation presents to development of economic relations between nations Treaties or Conventions are thus instruments signaling sovereign political choices negotiated between States to avoid double taxation through restriction of tax claims in areas where overlapping tax claims are expected, or at least theoretically possible 7

Leading International Tax models and commentary OECD Model Tax Convention on Income and on Capital United Nations Model Double Taxation Convention between Developed and Developing Countries United States conventions Klaus Vogel on Double Taxation Convention A Commentary to the OCED, UN and US Model Conventions Philip Baker on Double Taxation Convention 8

Adjudicating Forums in India High Court / Supreme Court Tribunal Mutual Agreement Procedure Advance Pricing Agreement Authority of Advance Ruling Settlement Commission Union Cabinet 9

Adjudicating Forums not available in India Arbitration (Article 25 of the OCED and UN Convention) 10

Treaties and Domestic Law: A Synergy An interplay exists between treaties and the statute governing income tax in India. S.90 of Income Tax Act, 1961: delegated & valid legislation Mini legislations Binding on parties Conflict between law and treaty which prevails? Application of treaties optional to taxpayer 11

Basic Treaty Principles Treaty commitments must be honored by the parties in good faith A party may not invoke the provisions of its internal law as justification for its failure to honor its treaty commitments A treaty should be interpreted in good faith in accordance with the ordinary meaning of its terms, in their context and in light of its object and purpose 12

Interpretation of Treaties vs. Domestic Law Principles adopted in interpretation of Treaties are not the same as those in interpretation of Statutory Legislation . Treaties are negotiated and entered into at a political level and have several considerations as their bases . Treaty interpretation should be holistic Indian Supreme Court Decision Union of India vs Azadi Bachao Andolan (2003) 13

General rule of interpretation [Article 31] 1. A treaty shall be interpreted in good faith in accordance with the ordinary meaning to be given to the terms of the treaty in their context and in the light of its object and purpose. 2. The context for the purpose of the interpretation of a treaty shall comprise, in addition to the text, including its preamble and annexes: (a) any agreement relating to the treaty which was made between all the parties in connection with the conclusion of the treaty; Ram Jethmalani v.s Union of India 339 ITR 107(SC) 14

Article 4: Residence International legal concept Concept of Fiscal Domicile Right to tax sufficient exercise of that right irrelevant Azadi Bachao Aandolan 263 ITR 706(SC) 16

International Tax Treaties Basic Concepts Concept of Person A person must be Resident namely Liable to tax in other contracting state this is determining factor for treaty entitlement Treaty relief is available to persons who are resident Article 3(2) effect of domestic law in interpretive process 17

International Tax Treaties Basic Concepts Article 3(3) of the India UK DTAA As regards the application of this Convention by a Contracting State any term not otherwise defined shall, unless the context otherwise requires, have the meaning which it has under the laws of that Contracting State relating to the taxes which are the subject of this Convention. 18

Liable to tax Union of India v. Azadi Bachao Andolan 263 ITR 706 (SC) Serco BPO Pvt Ltd. V. AAR 280 CTR 1 (P&H) Emirates Shipping Line, FZE v. ADIT 349 ITR 493 (Del) ADIT v. Green Emirate Shipping & Travels 100 ITD 203 (Mum) Maerskline UK Ltd v. DDIT WP Nos.1295/2008 & 272/2009 (Cal HC) 19

Heads of Income under Treaties Income from Immovable property Article 6 Business Income Article 7 Shipping and Airline Business Article 8 Dividend Article 10 Interest Article 11 Royalty Article 12 Capital Gains Article 13 Income from Employment Article 15 Directors Fees Article 16 Artists and Sportsperson Article 17 Pension Article 18 Government Service Article 19 Students Article 20 Other Income Article 21 20

Articles allowing source based taxation Income from Immovable property Business Income (if PE) Interest / Royalty / FTS (if arising or payer is in source jurisdiction) Capital Gains Situs of immovable property / Movable property if part of PE Co-owns shares residence of shareholders* Shares of a company deriving more than 50 per cent* of its value from immovable property 21

Article allowing residence based taxation Business Income If no PE Shipping / Airline Capital gains owner of shares in resident state* 22

Mauritius conundrum How was the problem created Who is responsible for treaty shopping CBDT Circular No 682 dated 30 March 1994 CBDT Circular No 789 dated 13 April 2000 Press Release dated 1 March 2013 General Anti Avoidance Rules (GAAR) deferred till FY 2017-18 (to apply prospectively to investments made on or after 1 April 2017) 23

Union of India v Azadi Bachao Andolan 263 ITR 706 Supreme Court Issue Whether Circular No. 789 dated 13.4.2000 with regard to the application of Indo Mauritius Double Taxation Avoidance Convention issued by the CBDT is ultra vires of S.90 and S.119 of Income Tax Act, 1961? Held Principles adopted in interpretation of Treaties are not the same as those in interpretation of Statutory Legislation Treaties are negotiated and entered into at a political level and have several consideration as their bases Circular briefly defines Article 4 of the Indo Mauritius DTAC and states that FIIs and other investor funds incorporated in Mauritius are invariably residents of the country and thus liable for taxation in Mauritius. SC states that Circular No. 789 does not interfere with S. 90 and S. 119 and is well within the ambit of the Indian Income Tax Act 24

Article 5 : Permanent Establishment Fixed place of the business of an enterprise in a particular country. Types of PE include Fixed Place PE Agency PE Service PE Construction PE PE excludes those places where activities involved include: Ancillary services Storage facilities or display of merchandise Maintenance of fixed place of business for supply of information 25

Article 23 : Methods for Elimination of Double Taxation Aims to do away with double taxation. Methods adopted to eliminate double taxation: (i) Exemption Method (Full exemption/exemption with progression State of Residence will not tax the income which has been earned and taxable in the State of Establishment (ii) Credit Method (Full credit/Ordinary credit) State of Residence will calculate tax on the entity s total income in State of Establishment and permits a credit for tax paid in the other state 26

Article 25 : Mutual Agreement Procedure (MAP) Dispute resolution mechanism adopted for resolving differences out of interpretation of the Convention Efficient and flexible tool; provides for co- operation Dispute resolution mechanism adopted for resolving differences out of interpretation of the Convention Efficient and flexible tool; provides for co-operation MAP could be invoked if an individual believes that the actions of the Contracting State would result in taxation not in accordance with Convention provisions Competent authorities shall resolves any doubts pertaining to the interpretation and application of the Convention MAP guidelines are binding on tax authorities of both the Contracting States, if accepted by the assesse 27

Article 26 : Exchange of Information Device adopted to enhance tax clarity and crackdown on fiscal evaders with aid of State cooperation Competent authorities in the Contracting States can share certain specified information with respect to Convention Domestic law governing taxation Necessary to prevent fraud and/or evasion of taxes. Generally, such information is secret and cannot be disclosed Information can be made public once it has been disclosed in court proceedings 28

Retrospective amendments To be or not to be... 29

Retrospective to be or not to be Section 90 has been amended by the following Finance Act(s) Finance (No 2) Act 2009 Finance Act 1972 Finance (No 2) Act 1991 (w.r.e.f. 1-4-1972) Finance Act 2001 (w.r.e.f. 1-4-1962) Finance Act 2003 Finance (No.2) Act 2004 (w.r.e.f. 1-4-1962) Finance Act 2013 Finance Act 2012 (Explanation-3 w.r.e.f. 1-10-2009) 30

CIT v. P.V.A.L. Kulandagan Chettiar 267 ITR 654 (SC) Income from immovable property situated in Malaysia may be taxed only in that contracting state 31

Notification No 91 of 2008 dated 28/08/2008 defines the expression may be taxed Wherever the term may be taxed occurs in any DTAA has to be understood as chargeable under the domestic law, subject only to any relief in accordance with the provisions of the agreement 32

Asia Satellite Telecommunications Co. Ltd v Director of Income Tax 332 ITR 340 Delhi High Court Issue Whether amounts received by the telecommunications company from its non resident customers for availing transponder capacity was subject to tax if the company s revenue fell under the category of S.9 (1) (vi) of the Act? Held AsiaSat does not have a presence or business connection with India mere satellite footprint and transponder in orbit does not constitute presence of business operations in India. Signals were uplinked and down linked from abroad. Transponder inseparable from the satellite. Process in receiving and retransmitting signals is inseparable from the process of the satellite. AsiaSat was the operator of the satellites and had not leased the satellites to its customers, thus its earnings could not be classified as royalties and taxed u/s 9(1)(vi) of the Act. OECD and Klaus Vogel Commentary use of satellite is a service and not a rental 34

Sanofi Pasteur Holdings SA 354 ITR 316 Andhra Pradesh High Court Issue Whether the gain arising out of alienation of shares of a French subsidiary (having underlying shares in an Indian co) by a French Holding company (seller) to another French company (buyer) be liable to tax in India under the treaty between India and France? Held French subsidiary company is a distinct entity of commercial substance Article 14(5) does not contemplate a see through unlike Article 14(4) dealing with immoveable property. Retrospective amendments in domestic law do not apply to a treaty in absence of a clear non obstinate clause Meaning of any term not defined in Treaty can have the meaning under the similar domestic law unless the context otherwise requires Taxation right allocated to France under the DTAA 35

Verizon Communication Singapore Pte Ltd (33 Taxmann Com 70 (MAD) Issue: Whether payment received by Verizon engaged in the business of providing international connectivity services amounts to payment for royalty (or not) under the treaty between India and Singapore? Held: Payments amount to royalty both under domestic law and treaty between India and Singapore Services involves use of equipment and hence triggers equipment royalty Alternatively, it also amounts to royalty for use of process 36

Serco BPO Pvt Ltd. V. AAR, 280 CTR 1 (P&H) Issue Whether the capital gains arising in the hands of two Mauritius based 'Seller companies' on account of the sale of shares of an Indian company is not chargeable to tax under India Mauritius DTAA read with Section 90(2) of the Income Tax Act, 1961? Held Not a single finding of fact in relation to the primafacie finding of the AAR that the transaction/arrangement in this case was designed for avoidance of income tax in India In view of the circular 789, it is incumbent upon the authorities in India to accept the certificates of residence issued by the Mauritian authorities Once authenticity of the TRC is not disputed, a failure to accept the TRC issued by the Mauritian authorities would be an indication of breakdown in the faith reposed by the Government of India in the Government of Mauritius and the Mauritian authorities reiterated in and evidenced by statutory Circulars issued under section 119 of the Act Taxation right allocated to France under the DTAA. Capital gains arising from the sale of the shares was held liable to tax only in Mauritius 37

And few more Director of Income Tax v/s Nokia 358 ITR 259 (Del) Amendments to the Act cannot be read into the treaty Director of Income Tax v/s TV Today Network 221 Taxman 123 (Del) In view of explanation 5 & 6 to section 9(1)(vi) which were inserted retrospectively by the Finance Act, 2012 receipts earned from providing data transmission services through satellite is to be considered as royalty 38

What is Transfer Pricing? Ascertaining the price charged in transaction between related enterprises/entities of Tangible assets Intangible assets Controlled services Financial arrangements 40

What is Transfer Pricing? Three key concepts International transaction or Specified domestic transactions 1 Associated Enterprise (AE) 2 Arm s Length Price (ALP) 3 41

Why is important? Deterrence to international transactions resulting into shifting of profit and over all low tax payment by MNE s in various jurisdictions Sharing of pie between jurisdictions 42

Stakes Involved.. (allegedly) INR figures in crore FY 2004-05 1,220 FY 2005-06 2,287 FY 2006-07 3,432 FY 2007-08 1,614 FY 2008-09 6,140 FY 2009-10 10,908 FY 2010-11 23, 237 FY 2011-12 44,531 FY 2012-13 70,000 approx* FY 2013-14 60,000 approx* 43

Methods of Transfer Pricing Comparable Uncontrolled Price Method (CUP) Resale Price Method (RPM) Cost Plus Method (CPM) Profit Split Method (PSM) Transactional Net Margin Method (TNMM) Any other method that may be prescribed by the Board 44

Income attibution 2 step process Functions Assets Risk (FAR) Analysis of the entity Comparability Analysis in order to find out the Arm s Length Price of the transaction in an Uncontrolled manner 1 2 45

Intangibles Intangibles Whether any exists? What is that intangible? Who has developed/created that intangible? Who owns that intangible? What is the correct value of that intangible? 46

Major Decisions on Transfer Pricing 47

Vodafone India Services (Bom HC) [2014] 50 taxmann.com 300 Issue: Issuance of Equity Shares by Indian company to its foreign parent The issue of shares at a premium is a capital account transaction and not income Issue of shares does not give rise to any income from an admitted International Transaction. Thus, no occasion to apply Chapter X of the Act can arise in such a case Maersk Global Centres (India) (P.) Ltd. [2014] 43taxmann.com100 (Mum - SB) Issues: 1) Comparability between low-end BPO s and high-end KPO s & 2) Use of a abnormally high profit margin as a comparable Classification of ITES into low-end BPO services and high-end KPO services for comparability analysis would not be fair and proper TP Regulations in India deviate from OECD and specify the Arithmetic Mean for determining the ALP and not interquartile range Abnormally high profit margin comparable should trigger further investigation in order to establish whether it can be taken as comparable or not 48

Li & Fung [40 Taxmann.com 300 (Del)] Issue: Relevant cost to calculate net profit margin under TNMM The ALP can t be determined on the basis of FOB value IT Act draws heavily from the OECD Model Tax Convention interpretation under article 9 The study carried out by the assessee must first be rejected, for any further alterations to take place Once TNMM was deemed as the most appropriate method, the distortions, if any, had to be addressed within its framework EKL Appliances Limited [2012] 345 ITR 241 [Delhi] The tax authorities cannot question the commercial rationale of legitimate business expenses incurred by the taxpayer as long as it is demonstrated that the transaction is at arm s length Reliance on the OECD Transfer Pricing Guidelines 49

")

")

")

")

")