OECD BEPS Project: Impact Assessment and Survey Findings

Explore the journey of the OECD's BEPS project, from its inception in 2013 to the endorsement of final reports in 2015. Learn about the purpose of the survey conducted to gauge the project's impact on members, taxpayers, and governments. Discover the approach taken in analyzing the 15 Action items and identifying the likely effects on tax jurisdictions.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

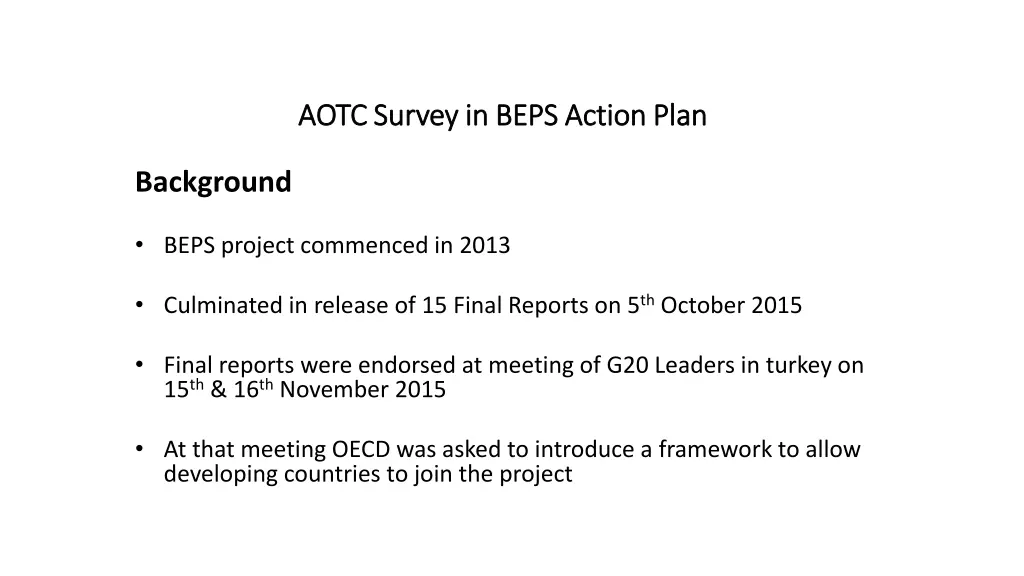

AOTC Survey in BEPS Action Plan AOTC Survey in BEPS Action Plan Background BEPS project commenced in 2013 Culminated in release of 15 Final Reports on 5thOctober 2015 Final reports were endorsed at meeting of G20 Leaders in turkey on 15th& 16thNovember 2015 At that meeting OECD was asked to introduce a framework to allow developing countries to join the project

OECD holds the first Asia-Pacific Technical Meeting in Yogyakarta, Indonesia to discuss challenges in the region in implementing BEPS, on going development and monitoring the measures adopted Twelve countries represented in AOTC attended that meeting BEPS has been a theme in the past two AOTC conferences and continues as the theme in 2016 in Hong Kong Before the 2015 Osaka conference General Council endorsed the survey proposed by the Technical Committee to gain members response to the Final BEPS reports

Purpose of the Survey Gauge the affect the OECDs work is having on members, taxpayers, tax authorities and Government Provide information to allow AOTCA to make meaningful contributions to the tax policy debate Obtain an understanding of the relevant tax legislation and issues concerning member s tax jurisdictions Identify issues specific to jurisdictions Allow the Technical Committee to consider the impact of OECDs BEPS project on the Asia Pacific region as a whole

Approach to the Survey Distil the information in the 15 Action items and design questions to produce sufficient information about the likely impact on members and their jurisdictions Under each of the 15 Action items somewhere between 5 to 8 questions were asked

Example Action 7: Prevent the artificial avoidance of PE status This Action item addresses: (a) Commissionaire (or dependent agent) arrangements; (b) Specific exemptions, in particular preparatory or auxiliary activities; (c) splitting-up of contracts ("anti-fragmentation" rules). Essentially the recommendations are directed at updating the Model Treaty to embrace modern strategies for avoiding PE status. Commissionaire arrangements might be addressed by including such arrangements as a PE where a person acting on behalf of an enterprise habitually engages with specific persons in a way that results in the conclusion of contracts with an exclusion for genuinely independent agents.

Questions 7.1 Are Commissionaire arrangements common in your country? 7.2 If they are, do your domestic legislation and treaty terms address the concerns raised in the OECD report already? 7.3 If the answer to question 7.2 is no, would the suggestions made in the final report adequately address the issue for your country? 7.4 Do your domestic legislation and treaties presently have a specific exemption for preparatory or auxiliary activities?

7.5 If the answer to question 7.4 is yes, does the exemption pose BEPS problems for your country? 7.6 Would the OECD suggestions for remedying the exemption problem work in your country? If not, why not? 7.7 Is fragmentation of contracts, as described in the Action 7 report, an issue of practical concern in your country? If not, why not? 7.8 If the answer to question 7.7 is yes, would the recommendations for remedying fragmentation resolve the concern? If not, why not? 7.9 What impact would adoption of all or any of the OECD suggestions have on tax practitioners in your country?

Responses The responses were collated and summarised on a country by country basis Example Action 7: Prevent the artificial avoidance of PE status Malaysia Commissionaire arrangements are not common. There is no domestic or treaty provisions to address such arrangements. Currently there is an exemption for preliminary or auxiliary activities. Artificial fragmentation of contracts is a concern.

Hong Kong Commissionaire arrangements are not common. There are no domestic or treaty provisions to address such arrangements. Hong Kong taxes only profits sourced domestically and has an operations test to determine source. Preparatory and auxiliary activities are not relevant to determining where the operations are carried out. A preparatory or auxiliary activities exemption could be contrary to the present testing requirement. Fragmentation of contracts is not common.

Australia Commissionaire arrangements are not common in Australia. The newly introduced multi-national anti-avoidance provision ( MAAL ) may combat such arrangements. There is a specific exemption for preparatory or auxiliary activities. It is not clear how large a problem is presented by the exemption. Not clear whether fragmentation of contracts is a material concern. There will be issues arising when treaties are being negotiated with reconciling the treaty provisions with the MAAL.

China Commissionaire arrangements are not common. Dependent agent arrangements are more frequently used. The OECD treaty provisions are widely adopted in China s treaty network. There is an exemption for preparatory or auxiliary activities. There are some companies taking advantage of fragmentation of contracts and which may be resolved by adopting the OECD recommendation.

Taiwan Commissionaire arrangements are common in Taiwan. As Taiwan adopts the OECD current model treaty there are no provisions governing artificial avoidance of PE status. In a recent case a representative team of a Singapore online service company was found to be a PE for the purposes of the Taiwan-Singapore treaty based on a substance over form approach. Contract fragmentation is used to avoid PE status in Taiwan. PPT is regarded as a practical approach in Taiwan

Singapore Commissionaire arrangements are not common. Agency arrangements are more common. A commissionaire arrangement is likely to be treated as a principal carrying on business through a dependent agent/ The issue in Singapore is whether the income is sourced there rather than the existence of PE. Treaties contain an exemption for preparatory or auxiliary activity (following the OECD model). A representative office can undertake preparatory or auxiliary activities under the domestic law without being treated as carrying on a business but limited to 2 to 4 years. Fragmentation of contracts is not a major concern. The subjective nature of the tests recommended by the OECD is likely to create greater uncertainty for taxpayers.

Japan Commissionaire arrangements are common. There is exemption for preparatory or auxiliary activities in the domestic law and most treaties. Fragmentation of contracts is a concern in Japan and may be addressed by the OECD recommendation.

General Regional Observations Commissionaire arrangements are not seen to be common place or of great concern in most jurisdictions apart from Japan [the accuracy of the Japanese observation needs to be checked]. Preparatory or auxiliary activities are exempt in almost all countries and do not appear to raise great concerns. Fragmentation of contracts is not a concern in all countries apart from Japan. The OECD recommendations would, if adopted, alleviate the problem.

Dissemination CFE IBFD OECD UN GTACF