Setting Standard Overhead, Analysis Methods, and Case Examples

Learn how to set standard overhead using predetermined rates, analyze overhead variances, and explore case examples to understand the impact of overapplied and underapplied overhead on Cost of Goods Sold (COGS).

Uploaded on | 0 Views

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

STANDARD COSTING OVERHEAD

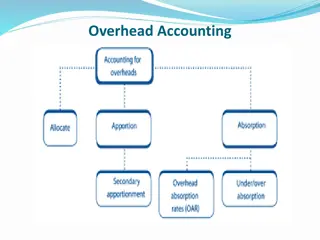

Bagaimana menetapkan Standar Overhead? Metode yang digunakan untuk menghitung dan menyusun standar overhead sama dengan penghitungan tarif predetermined dan dibebankan kepada produk/pesanan. Tarif standar overhead setiap departemen produksi atau pusat biaya adalah total anggaran overhead dibagi dengan total dasar alokasi yang telah ditetapkan sebelumnya. Dasar alokasi bisa berdasarkan biaya bahan baku, biaya tenaga kerja langsung, jam kerja langsung atau jam mesin, atau dasar lain yang relevan dengan obyek biaya.

Metode analisis varian overhead Analisis Satu Varian Analisis Dua Varian Overhead Variances Analisis Tiga Varian Analisis Empat Varian

Metode analisis varian overhead Analisis 1 Varian Analisis 1 varian merupakan varian antara BOP sesungguhnya dan BOP Dibebankan. Analisis 2 Varian Apabila BOP Sesungguhnya lebih besar daripada BOP Dibebankan maka akan muncul Underapllied Overhead yang berdampak pada peningkatan CGS. Overhead Variances Analisis 3 Varian Sebaliknya bila BOP Sesungguhnya lebih kecil dari BOP Dibebankan maka terjadi Overapplied Overhead yang berdampak pada penurunan CGS. Analisis 4 Varian

Contoh Kasus Applied Factory Overhead = $ 20,000 Factory Overhead Control = $ 15,000 Overhead variance = $ 5,000 (Overapplied Overhead) Favorable Applied Factory Overhead = $ 20,000 Factory Overhead Control = $ 25,000 Overhead variance = $ 5,000 (Underapplied Overhead) Unfavorable

Metode analisis varian overhead Analisis 1 Varian Controllable Variance = Actual Overhead Budgeted allowanced based on standard hours Analisis 2 Varian Overhead Variances Volume Variance = Budgeted allowanced based on standard hours standard Overhead Analisis 3 Varian Analisis 4 Varian

Contoh Kasus Monthly capacity : 80,000 direct labor hours Actual produced 38,000 units, Actual direct labor hours 77,500 Actual factory overhead $700,000. Variable overhead 2 hours@$6 = $12 Fixed overhead 2 hours @$3 = $ 6 Overhead per unit = $18 Unfavorable Unfavorable

Metode analisis varian overhead Spending Variance = Actual Overhead Budgeted allowanced based on actual hours Analisis 1 Varian Analisis 2 Varian Variable Efficiency Variance = Budgeted allowanced based on actual hours Budgeted allowanced based on standard hours Overhead Variances Analisis 3 Varian Analisis 4 Varian Volume Variance = Budgeted allowanced based on standard hours standard Overhead

Contoh Kasus Monthly capacity : 80,000 direct labor hours Actual produced 38,000 units, Actual direct labor hours 77,500 Actual factory overhead $700,000. Variable overhead 2 hours@$6 = $12 Fixed overhead 2 hours @$3 =$ 6 Overhead per unit = $18 Favorable Unfavorable Unfavorable

Metode analisis varian overhead Spending Variance = Actual Overhead Budgeted allowanced based on actual hours Analisis 1 Varian Variable Efficiency Variance = Budgeted Fixed Overhead (Actual Times x Fixed Overhead Rate) Analisis 2 Varian Overhead Variances Analisis 3 Varian Fixed Efficiency Variance = (Actual Times Standard Time) x Fixed Overhead Rate Analisis 4 Varian Idle Capacity Variance = Budgeted allowanced based on standard hours standard Overhead

Kesimpulan yang didapatkan dari Variance Overhead: semakin rinci analisis varian semakin akurat informasi yang didapatkan sebagai bahan pertimbangan corrective action.