Understanding Public Expenditure and Public Debt

Explore the classification and causes of public expenditure, budget types, public debt management, deficit concepts, and fiscal federalism issues. Learn about revenue vs. capital expenditure, productive vs. unproductive spending, transfer vs. non-transfer expenses, and more in this comprehensive guide.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

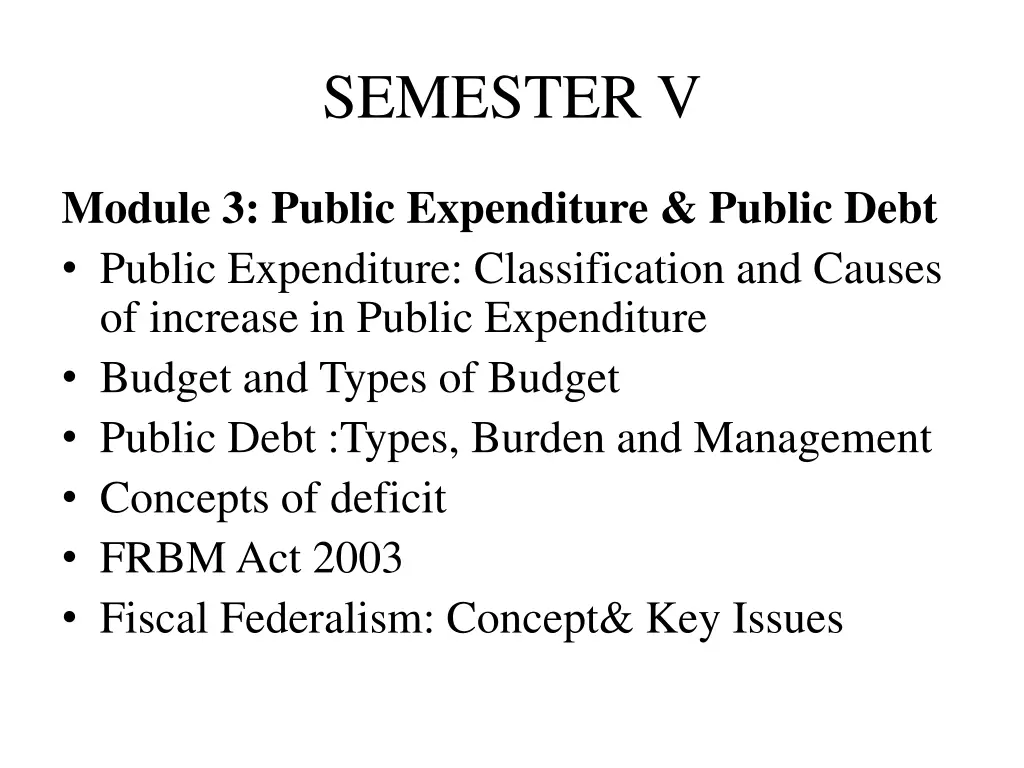

SEMESTER V Module 3: Public Expenditure & Public Debt Public Expenditure: Classification and Causes of increase in Public Expenditure Budget and Types of Budget Public Debt :Types, Burden and Management Concepts of deficit FRBM Act 2003 Fiscal Federalism: Concept& Key Issues

PUBLIC EXPENDITURE Public expenditure refers to the expenses of public authorities like the central, state and local governments. Public expenditure occupies a very important place in the study of public finance. It is the end of all financial activities of the government. It is incurred basically to maximize social welfare.

CLASSIFICATION OF PUBLIC EXPENDITURE Revenue & Capital Expenditure Productive & Unproductive Expenditure Non-Transfer & Transfer Expenditure Plan & Non-Plan Expenditure Dalton s Classification

1. Revenue and Capital Expenditure Revenue Expenditure 1. The expenditure incurred in revenue account of the budget is called revenue expenditure. 2. It includes expenditure incurred for current flow of goods and services and to maintain capital stock intact. 3. It is known as current expenditure in the form of consumption. 4. It is incurred on civil administration, defence forces, public health, education, etc. 5. It is of recurrent type, which is incurred year after year. Capital Expenditure 1. The expenditure incurred in capital account of the budget is known as capital expenditure. 2. It is a long term investment expenditure done by the government. 3. It helps to increase productive capacity of the economy. 4. They are incurred on building durable assets like-highway, dams, irrigation project, buying machinery, etc. 5. They are non-recurrent type of expenditure.

2. Productive and Unproductive Expenditure Productive Expenditure 1. The expenditure, increases capacity of the country, is known as expenditure. 2. It helps to increase volume of output and employment in the country. 3. The expenditure establishment sector infrastructure devpt., devpt. of agriculture, roads, dams, railway, airport etc. Unproductive Expenditure 1. Unproductive expenditure is an expenditure, which does not increase capacity of a nation. 2. The expenditure, which does not create as asset, is known as unproductive expenditure. 3. Expenditure in the form of defence, maintenance of law and order, interest payment, administrative expenses which the productive productive productive on of public industries,

3. Transfer and Non-transfer Expenditure Transfer Expenditure 1. Transfer expenditure is that expenditure which involves the transfer of income from one person to another. 2. It is done government on pension, unemployment allowances, benefit, welfare benefits, interest payment, public debt and subsidies, etc. 3. It does not involve creation of goods and services. Non-transfer Expenditure 1. The expenditure done by the government to create output and income in the country is known as expenditure. 2. They are buying or using goods and services, these expenditure education, public health etc. 3. It uses productive resources and generates employment and income directly in the country. non-transfer by the incurred for sickness include defence, on

4. Plan and Non-plan Expenditure Plan Expenditure 1. The expenditure incurred by the government for development which are outlined in the ongoing five year plan. 2. Plan expenditure is one, which is provided in the budget. 3. This expenditure is called as expenditure promotes economic growth and development Non-plan Expenditure 1. Non-plan expenditure refers to that expenditure which is not included in the ongoing five-year plan. 2. Non-plan expenditure does not have any provision in the budget. 3. It consists development and thus termed as non- development expenditure. schemes, of expenditure non- development because it

5. Daltons Classification of Public Expenditure a) Expenditure on political executive: Expenditure on ceremonial heads of state. b) Administrative expenditure:- government departments and offices etc. c) Security expenditure:- Expenditure on defence. Expenditure on administration of justice. d) Development expenditure. e) Social expenditure:- Expenditure on public health, community welfare, social security, education etc. Expenditure on

Causes of Growth of Public Expenditure in India The size of public expenditure has been rising in both developed and developing countries due to increased in governmental functions both intensively and extensively. Increase in public expenditure has been explained by Wagner s Law and Wiseman-peacock Hypothesis. Wagner s Law: Adolf Wagner observed that there are tendencies for activities of the government to increase both intensively and extensively. Wiseman-Peacock Hypothesis: According to this hypothesis, public expenditure does not increase at a steady continuous rate but in a step like manner.

Causes of Growth of Public Expenditure in India 1. Expansion of traditional functions: Traditionally, the government is essential to undertake activities like defence, administration, maintenance of law and order, etc. In recent time the role of government in this area has increased due to international pressure, efficiency in administration to meet to increasing demand of the community have pushed up defence and administrative expenses.

Causes of Growth of Public Expenditure in India 2. Welfare State: The modern government is considered to be a welfare state, where the government has to undertakes various welfare activities like public health, social insurance, education, upliftment of weaker sections, etc. to achieve economic and social well being of all. 3. Population: In 1951, India s population was 36 crore. It rose to 121 crore in 2011. With this growth in population has made it essential for the government to spend infrastructure, subsidies programmes. on education, and health, development

Causes of Growth of Public Expenditure in India 3. Rise in National Income: Rise in public expenditure leads to rise in NI and PCI. As a result, demand for public goods like education, communication, transportation, health care etc. tend to increase. Thus, government are expected to spend more on such goods. 4. Urbanisation: Since independence, the percentage of urban population has increased in this country from 17.3 percent in 1951 to 27.8 percent in 2011. As a result government has to spend not only on creating new infrastructure for cities but also on the maintenance and replacement of such infrastructure.

Causes of Growth of Public Expenditure in India 5. Subsidies: The government gives subsidies to different sectors in order to make essential goods and services affordable to the poor. Subsidies are also given to promote sectors like exports, Small scale enterprises, etc. In India Central govts. Subsidies have increased from Rs.9,581Cr. to Rs.1,04,181Cr. between 1991 and 2011. 6. Development Programmes: The govts. of India has to made huge expenditure in various physical and social infrastructure projects like Bharat Nirman, National Highways, Sarva Shiksha Abhiyan.

Causes of Growth of Public Expenditure in India 7. Poverty Alleviation and Employment Generation: Under Five years plans, the govts. has launched several schemes such as NREG to remove problems of poverty and unemployment, which requires continuous expenditure. 8. Servicing of Public Debt: Capital expenditure of the govts. have been financed through public debt. There has been a continuous growth in the total outstanding debt of the govts. As a result, public debt rose sharply from 41.6 % of GDP in 1980-81 to 56.7 % of GDP in 2009-10.

Causes of Growth of Public Expenditure in India 9. Administrative administrative machinery is large and has expanded many fold over the period. As a result, administrative expenditure has increased on maintenance of various ministries, depts. and offices, payment of salaries. 10.Democracy: India is the world s largest democracy. Periodic elections and maintenance of the political representatives have increased public expenditure to a great extent over the years. Machinery: Indian govts.

PUBLIC DEBT Public debt implies the borrowings by the government from banks, business organizations and individuals. Public debt may be defined as, financial obligations accepted by the government by way of raising loans or funds, either within or outside the country for financing public activities. In India, public debt consists of government treasury bills, post office savings certificates, national savings certificates, public provident funds etc. Public debt may be raised internally from individuals, banks and financial institutions or externally from international financial institutions like IMF, World Bank or from the advanced countries of the world.

1. Productive and Unproductive Public Debt Productive Debt 1. Debt raised by the government for some productive purpose like investment in economic and social infrastructure. 2. It helps to productive capacity of country. 3. It helps employment and income which further builds up the repayment capacity of the nation. 4. They are less burdensome on a nation. Unproductive Debt 1. Debt taken for unproductive purposes like financing war, famine relief, maintenance of law and administration etc. 2. It does not help to increase the productive capacity country. 3. It does not help to generate employment, repaying capacity of a country. 4. They are more burdensome on a nation. order, public increase the to generate of a income and

2. Compulsory and Voluntary Public Debt Compulsory Public Debt 1. It refers to that debt which is taken by the government from the public by applying some force. 2. They are raised government during financial emergency or Circumstances like war. 3. Under compulsory individuals, organizations and banks and financial institutions have to compulsorily subscribe to the government. Voluntary Public Debt 1. When the government raises loans through securities and bonds. 2. They are taken by the government times to finance activities. 3. People are subscribe to them and there is usually no involved. by the during normal various exceptional, voluntarily debt business compulsion

3. Internal and External Debt Internal Loans 1. Internal loans are raised within the country and subscribed mainly by its own citizens. 2. They are repayable in the domestic currency 3. They may be either voluntary or compulsory. 4. There is no direct money burden of such debts. External Loans 1. External loans are raised in foreign countries international institutions like the IMF, IBRD. 2. They have to be repaid usually in foreign currency. 3. They are usually voluntary. 4. They result in direct money burden. or financial from

4. Short term and long term debt Short term debts 1. They mature within one year duration. 2. The rate of interest is low on such loans, for e.g., 91-day day 182-day treasury bills. 3. The purpose of such debts is to meet revenue and expenditure shortfalls. Long term debts 1. They have a maturity period of one year or more. 2. The rate of interest is high on such loans for e.g., market borrowing and bonds. 3. The purpose of such debts is investment in economic and social infrastructure.

5. Redeemable and Irredeemable debt Redeemable debt 1. They are repaid at some specific future date. 2. The govts. arrangement for repayment of interest and principal amount within a specific period. 3. Most debts are redeemable in nature. Irredeemable debt 1. They do not have any definite date for final repayment. 2. The interest payments on such debts are made regularly. 3. Such borrowings are not very common. has to make

6. Funded and Unfunded debt Funded debts 1. They are repayable within a short period of time, usually one year. 2. They are generally taken to meet current needs like meeting temporary revenue deficits. Unfunded debts 1. They are long term debts. 2. They are taken by the govts. For building economic infrastructure. social and

Burden of Public Debt Internal Debt External Debt 1. Direct Real Burden 2. Indirect Real Burden 3. Burden on Future Generation 4. Effect on Private Investments 5. Effects on Capital Expenditure 6. Inflation 1. Direct Money Burden 2. Direct Real Burden 3. Indirect Real and Money Burden 4. Burden of Unproduc- tive Foreign Debt 5. Foreign Currency Burden 6. Domination of Creditor Country

BURDEN OF INTERNAL DEBT Internal public debts are raised and repaid within the country. Therefore, they have no direct money burden. The government taxes some people to repay the interest and the principal to the creditors. Such debts give rise to real burden.

BURDEN OF INTERNAL DEBT 1. Direct Real Burden: Transfer of purchasing power will take place as the government imposes tax to repay the internal debts. When purchasing power is transferred from the tax payers to the public creditors, it will influence the distribution of income in the country. Most developing countries depend more on indirect taxes than direct taxes. Indirect taxes are regressive nature, i.e. they impose greater burden on the relatively poor than the rich.

BURDEN OF INTERNAL DEBT 2. Indirect Real Burden: High rates of taxation generally have a negative effect on people s ability and willingness to work, save and invest. This in turn will affect productivity, production and investment in the economy. 3. Burden on Future Generation: It is usually the older generation who subscribe to govts. bonds and securities with their accumulated wealth. But the debts are repaid through taxes which are paid by the younger generation.

BURDEN OF INTERNAL DEBT 4. Effect on Private Investments: Most people believe that govts. Securities offers high interest rates and a safe place to invest their money. This reduces funds available for the private sector. One rupee investment by the govts. reduces the private investment by one rupee.

BURDEN OF INTERNAL DEBT 5. Effect on Capital Expenditure: In most developing countries including India, public debt is used to meet revenue deficit. A very large portion of govts. Revenue is spent on paying interests. Thus the govts is unable to make adequate capital expenditure on devpt. of infrastructure. 6. Inflation: If indirect taxes are raised in order to repay internal debts, then inflation may take place. Inflation reduces the real income or purchasing power of the poor.

BURDEN OF EXTERNAL DEBT External debt implies borrowing from foreign countries. It allows inflow of resources from foreign country to domestic country. But the repayment of external debt leads to taxation and transfer of resources from the domestic country to the foreign country. The burden of external debt is analysed below:

BURDEN OF EXTERNAL DEBT 1. The direct money burden: It is equal to the sum of principal and interest amount paid to external creditors. The sizes of the burden depend on the rate of interest and the amount of loan taken. 2. The direct real burden: It is measured in terms of the loss of welfare suffered by people of the debtor country due to repayment of debt. If the rich people are made to pay, the real burden will be smaller than if they are made mainly by the poor.

BURDEN OF EXTERNAL DEBT 3. The indirect money and real burden: This may be measured in terms of effects on production and allocation of resources. It arises from the check on productive capacity of the people either due to the imposition of taxes to meet public debt services charges or due to check on public expenditure. 4. Burden of unproductive foreign debt: If the external debt is used for unproductive purposes it will create a greater burden on the community.

BURDEN OF EXTERNAL DEBT 5. Foreign currency burden: The external debt has to repay in foreign currency which will increase the demand for foreign currency by debtor country's. This is likely to lead to decline in the exchange rate of debtor country which may lead to foreign exchange crisis causing a real burden. 6. Domination by creditor country: The creditor country may dominate the debtor country in various spheres. The debtor country may be forced to take decisions which may give more benefits to the creditor country.

CONCEPTS OF DEFICITS A public budget is a systematic estimate of government s revenue and expenditure for a period of one year. It shows the planned expenditure of the government and the expected revenue from taxes and other sources, during a given year. Receipts and expenditure are further divided into two parts namely: Revenue Budget: The revenue covers those items which are recurring in nature. It shows both revenue receipts, like taxes, surplus, income of public sector enterprises and revenue expenditure, like salaries to govts staff, subsidies, interest payments, etc.

Management of Public Debt Public debt is often a country s largest liability. Servicing of huge debt has led many countries into a depttrap , which takes away their resources which is essential for the economic development of the countries. Meaning Public debt management is the process of establishing and executing a strategy for managing the govt debt in order to raise the required amount of funding and to meet any other debt management goals of the govt, such as developing and maintaining an efficient market for govt securities.

Importance of Public Debt Management A good public debt management can help to reduce borrowing cost in many ways. A carefully balanced composition of securities can contain financial risk, which are harder to manage in countries having few alternative source of finance. It can also help to develop the domestic financial market and institutions due to availability of public debt instruments for investment and which can provide benchmarks for the pricing of other instruments. Prudent (cautious) debt management can make countries less vulnerable to contagion (contamination) and financial risks.

Framework for Public Debt Management 1. Debt Management Objectives and Co-ordination: The main objectives of debt management is to ensure financing needs and payment obligations are met at the lowest possible cost over medium term to long run. To achieve these debt managers, fiscal policy advisors, and central bankers should share an understanding of the objectives of debt mangt, fiscal and monetary policies. In short there should be better co-ordination between them.

Framework for Public Debt Management 2. Transparency and Accountability: For prudent debt mangt objectives should be clearly defined and publicly disclosed and the measures of cost and risk explained. Further, the allocation of responsibilities among the Ministry of Finance, Central bank and debt agency should be disclosed.

Framework for Public Debt Management 3. Institutional Framework: There should be legal frameworks which clarify the authority to borrow, and issue new debt, invest and undertake transactions on behalf of the govt. 4. Debt Strategy and Risk Management: Debt strategy should be properly implemented and management of risk in the portfolio should be eased by changing the structure of debt.

Framework for Public Debt Management 5. Efficient Market for Govt Securities: It is essential to achieve a broad investor base by giving importance to cost and risk involved and treat equally every investor. The debt managers, central bank and Ministry of finance should work closely with market participants and regulators for the devpt of efficient market. 6. Broad Principles of Debt Management: i. Low interest cost of servicing debt ii. Satisfy the needs of investors iii. Co-ordination between public debt, fiscal and monetary policies iv. Funding of short-term debt into long-term debt

Framework for Public Debt Management Efficient Market for Govt Securities: It is essential to achieve a broad investor base by giving importance to cost and risk involved and treat equally every investor. The debt managers, central bank and Ministry of finance should work closely with market participants and regulators for the devpt of efficient market. Broad Principles of Debt Management: Low interest cost of servicing debt Satisfy the needs of investors Co-ordination between public debt, fiscal and monetary policies Funding of short-term debt into long-term debt

CONCEPTS OF DEFICITS Capital Budget: The capital budget includes one time receipts and expenditure of the govts. It includes capital expenditure on infrastructure building and repayment of loans and capital receipts like borrowing, recovery of loans and proceeds from investment. A public budget can be balanced, surplus or deficit.

CONCEPTS OF DEFICITS In India, the budget has always shown deficit. A deficit in the budget can have many implications for the economy and influence the process of policy making. 1. Revenue Deficit: It takes place when the revenue expenditure is more than revenue receipts. Revenue receipts come from direct and indirect taxes and other sources like fees, fines, surplus of public enterprises. Revenue expenditure are made on administration, defence, interest payments and subsidies. 2. Budgetary Deficit: It is defined as the excess of total budgetary expenditure over total budgetary receipts.

CONCEPTS OF DEFICITS 3. Fiscal Deficit: It is defined as the excess of total expenditure (TE), including net lending (NL = Loans Recovery) over revenue receipts (RR), plus external grants (EG), plus non-debt capital receipts (NDCR) include proceeds from disinvestment of public enterprises. In other words, fiscal deficit is the excess of total expenditure, excluding repayment of debt, over total receipts, excluding debt ca[ital receipts. GFD = (TE + N L) (RR + EG + NDCR) 4. Primary Deficit: It is equal to fiscal deficit minus interest payments. DPD = GFD Interest Payments

FISCAL RESPONSIBILITY AND BUDGET MANAGEMENT ACT 2003 The fiscal situation in India was deteriorated throughout 1980 s and reached to a peak level of crisis in the year1990-91. The fiscal deficit in 1990-91 was 6.6 percent of GDP while revenue deficit was as high as 3.3 percent of GDP. The primary deficit was 2.8 percent in the same period. The situation did not improve significantly. This further indicates deterioration in fiscal situation due to rise in burden of interest payments. This was one of the factors responsible for the BOP crisis in 1990-91.

FISCAL RESPONSIBILITY AND BUDGET MANAGEMENT ACT 2003 The central government appointed a committee on Fiscal Responsibility Legislation on Jan. 17, 2000 to look into various aspects of fiscal system and recommended a draft responsibility of the government . To ensure fiscal discipline the central government accordingly introduced fiscal responsibility and budget management bill in the parliament in Dec. 2000 with the primary objective of reducing the central government s deficits and debts. The fiscal responsibility and budget management act was passed and came into force on 5 July2004. legislation on fiscal

Objectives of the FRBM Act 2003 1. To set the limits on government borrowing, under a time bound programme. 2. Achieve zero revenue deficit, to achieve sufficient revenue surplus and bring down fiscal deficits. 3. Make government responsible to ensure long-term macro- economic stability. 4. To make government responsible to reduce burden of debt repayment on future generations and to adopt prudent debt management. 5. Improve the transparency in fiscal operations of the government.

Main Features of FRBM Act 2003 and FRBM Rules 2004 1. Reduction in Revenue Deficit:- Reduce revenue deficit by 0.5% of GDP or more at the end of each financial year beginning with 2004- 05. Revenue deficit should be reduced to zero within a period of 5 years ending with 31st March 2009. 2. Reduction in Fiscal Deficit:- Reduce fiscal deficit 0.3% of GDP or more at the end of each financial year starting with 2004- 05. Fiscal deficit should be reduced to 3 percent of GDP by the end of 2008-09.

Main Features of FRBM Act 2003 and FRBM Rules 2004 3. Borrowing from the RBI:- The central government should not borrow directly from the RBI with effect from 1st March 2006 except by way of advances to meet temporary shortage of cash. 4. Additional Liabilities:- The central government should limit the additional liabilities to 9 % of the GDP in 2004-05 and should reduce this limit to by one % point of GDP at the end of each financial year.

Main Features of FRBM Act 2003 and FRBM Rules 2004 5. Quarterly Reviews: - The Finance Minister should take quarterly review of receipts and expenditure, and should place the outcome report of review before the parliament. 6. Fiscal Transparency:- i. The central government should minimize secrecy in preparation of annual budget. ii. The central government should disclose the information relating to the significant changes in accounting standards, policies and practices as well as revenue arrears, guarantees and assets by 2006-07.

Main Features of FRBM Act 2003 and FRBM Rules 2004 7. Government Guarantees:- The central government should not provide guarantee to loans borrowed by the state governments and public sector undertakings in excess of 0.5% of GDP in any financial year beginning with 2004-05.