Understanding Retirement Benefit Plans

Discover the intricacies of retirement benefit plans, including defined contribution and defined benefit plans, their recognition, measurement, and disclosure requirements. Explore the obligations companies have in providing retirement benefits to their employees and how these plans are reported. Gain insights into the differences between defined contribution and defined benefit plans in post-employment benefits.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

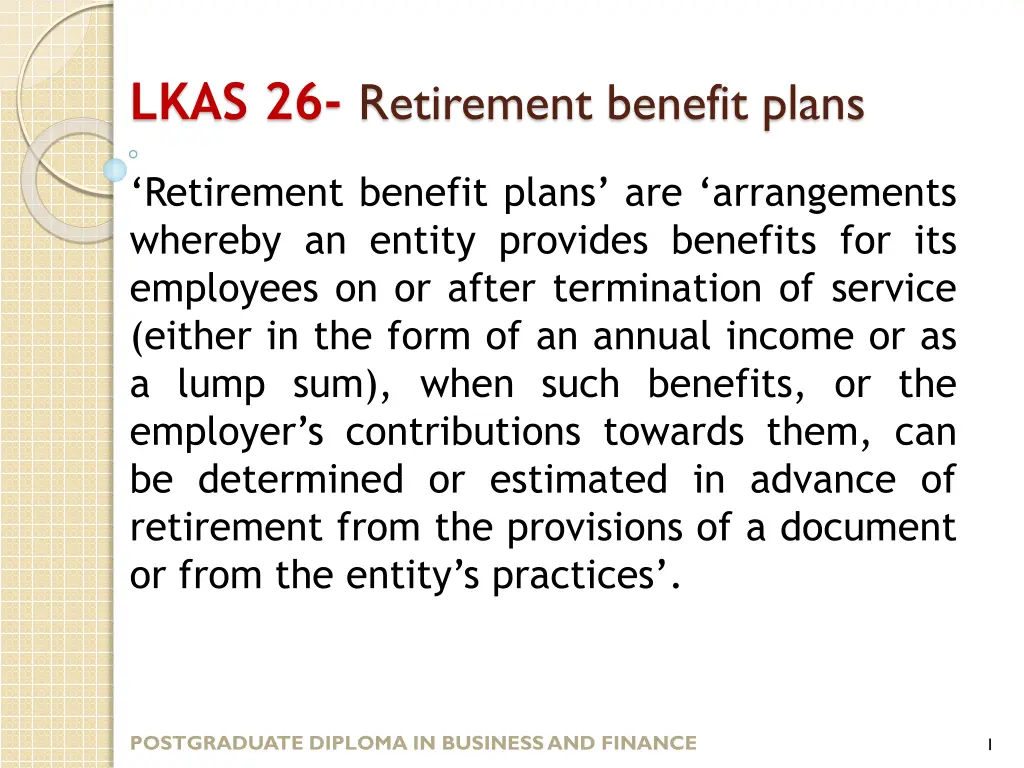

LKAS 26- Retirement benefit plans Retirement benefit plans are arrangements whereby an entity provides benefits for its employees on or after termination of service (either in the form of an annual income or as a lump sum), when such benefits, or the employer s contributions towards them, can be determined or estimated in advance of retirement from the provisions of a document or from the entity spractices . POSTGRADUATE DIPLOMA IN BUSINESS AND FINANCE 1

Retirement benefit plan Defined contribution plans. Retirement benefit plans whereby retirement benefits to be paid to plan participants are determined by contributions to a fund together with investment earnings thereon.

Companys only obligation is to pay agreed amount into plan Recognition and measurement Expense in the period Liability recognized for contributions unpaid at period end. Disclosure Disclose amount recognized as expense

Defined benefit plans. Retirement benefit plans whereby retirement benefits to be paid to plan participants are determined by reference to a formula usually based on employees earnings and/or years of service

Defined benefit plans - report The report of a defined benefit plan should contain either: A statement that shows the net assets available for benefits; the actuarial present value of promised (distinguishing between vested benefits and non-vested benefits) and the resulting excess or deficit retirement benefits A statement of net assets available for benefits, including either a note disclosing the actuarial present value of promised retirement benefits (distinguishing between vested benefits and non-vested benefits) or a reference to this information in an accompanying actuarial report

ex: Extract from Annual Report j) Employee benefits (i) Defined contribution plans A defined contribution plan is a post-employment benefit plan under which contributions are made into a separate fund and the entity will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution plan are recognised as an employee benefit expense in profit or loss in the periods during services is rendered by employees. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in future payments is available. Employee Provident Fund All employees of the Company are members of the Sri Lanka Telecom Provident Fund to which the Company contributes 15% of such employees basic salary and allowances. All employees of subsidiaries of the Group except for Sri Lanka Telecom (Hong Kong) Limited and SLT Services (Private) Ltd are members of Employees Provident Fund (EPF), to which respective subsidiaries contribute 12% of such employees basic salary and allowances. Employees of SLT Services (Private) Ltd are members of Employees Provident Fund (EPF), where the Company contribute 15% of such employees basic salary and allowances. Employee Trust Fund The Company and other subsidiaries contribute 3% of the salary of each employee to the Employees Trust Fund.

ii) Defined benefit plans A defined benefit plan is a post-employment benefit plan other than a defined contribution plan. The Group s net obligation in respect of defined benefit plans is calculated separately for each plan by estimating the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value. The valuation is performed annually by a qualified actuary using the projected unit credit method. When the valuation results in a benefit to the Group, the recognised asset is limited to the total of any unrecognised past service costs and the present value of economic benefits available in the form of any future refunds from the plan or reductions in future contributions to the plan. An economic benefit is available to the Group if it is realisable during the life of the plan, or on settlement of the plan liabilities. When the benefits of a plan are improved, the portion of the increased benefit relating to past service by employees is recognised in profit or loss on a straight-line basis over the average period until the benefits become vested. To the extent that the benefits vest immediately, the expense is recognised immediately inprofit or loss. The Group recognises all actuarial gains and losses arising from defined benefit plans directly in the other comprehensive income and all expenses related todefined benefit plan in personnel expense in profit or loss.

Defined benefit plans")