Update on Cross-Border M&A in Corporate/International Taxation

This update covers key discussions on cross-border M&A in corporate and international taxation, including PTEP and Section 961 Basis implications, IRS Notice 2024-16, and regulations to be issued for covered inbound transactions. The content delves into intricate scenarios involving basis adjustments and distribution implications for US corporations acquiring stock in controlled foreign corporations (CFCs).

Update on Cross-Border M&A in Corporate/International Taxation

PowerPoint presentation about 'Update on Cross-Border M&A in Corporate/International Taxation'. This presentation describes the topic on This update covers key discussions on cross-border M&A in corporate and international taxation, including PTEP and Section 961 Basis implications, IRS Notice 2024-16, and regulations to be issued for covered inbound transactions. The content delves into intricate scenarios involving basis adjustments and distribution implications for US corporations acquiring stock in controlled foreign corporations (CFCs).. Download this presentation absolutely free.

Presentation Transcript

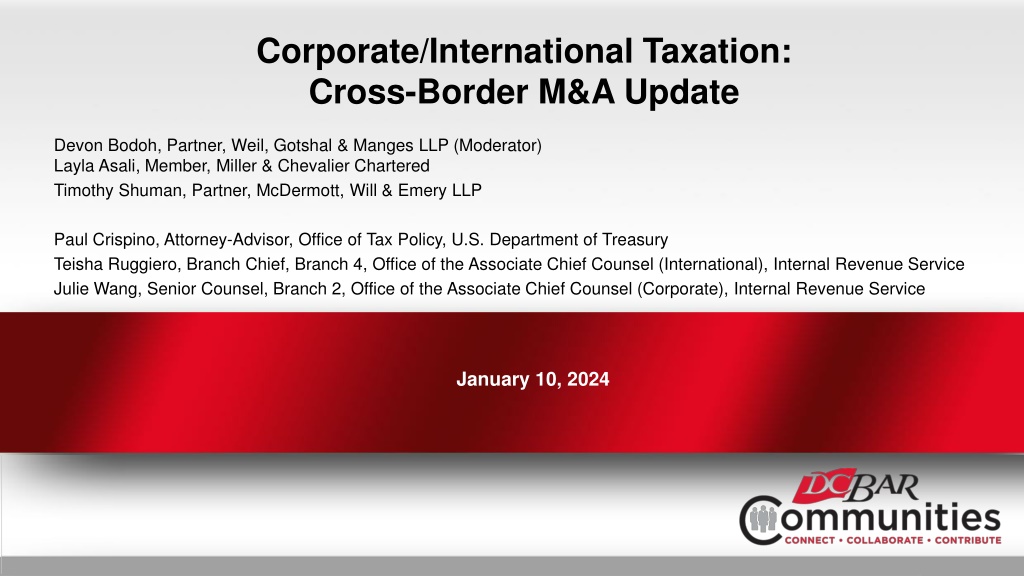

Corporate/International Taxation: Cross-Border M&A Update Devon Bodoh, Partner, Weil, Gotshal & Manges LLP (Moderator) Layla Asali, Member, Miller & Chevalier Chartered Timothy Shuman, Partner, McDermott, Will & Emery LLP Paul Crispino, Attorney-Advisor, Office of Tax Policy, U.S. Department of Treasury Teisha Ruggiero, Branch Chief, Branch 4, Office of the Associate Chief Counsel (International), Internal Revenue Service Julie Wang, Senior Counsel, Branch 2, Office of the Associate Chief Counsel (Corporate), Internal Revenue Service January 10, 2024

PTEP and Section 961 Basis: IRS Notice 2024-16 3

PTEP and Basis Example Inbound Section 332 Liquidation Year 1: $100 GILTI inclusion attributable to CFC2 creates $100 PTEP Section 961(a): $100 basis increase in CFC1 stock Section 961(c): $100 basis increase in CFC2 stock for purposes of section 951 USP End of Year 1: CFC1 distributes all assets to USP in a section 332 liquidation 1 CFC1 Liquidation CFC1 Year 2: CFC2 distributes $100 PTEP to USP 2 $100 Distribution What is USP s basis in CFC2 stock after the Year 1 section 332 liquidation of CFC1? Does section 961(c) basis in CFC2 stock become section 961(a) basis? CFC2 $100 PTEP Does USP recognize gain on distribution of PTEP by CFC2 in Year 2? Similar questions if CFC1 transfers assets to USS in an inbound F reorganization 4

PTEP and Basis IRS Notice 2024-16 Regulations to be Issued IRS Notice 2024-16 announces that forthcoming regulations will provide that, in the case of a covered inbound transaction, a domestic acquiring corporation s adjusted basis of the stock of an acquired CFC determined under section 334(b) or 362(b) is determined as if the transferor CFC s section 961(c) basis were adjusted basis. Section 961(c) basis must be with respect to the domestic corporation that acquires the stock of the acquired CFC in a covered inbound transaction Taxpayers may rely on the rules in Notice 2024-16 for transactions completed on or before the date proposed regulations governing the basis consequences of covered inbound transactions are published Comments due February 26, 2024 5

PTEP and Basis IRS Notice 2024-16 Covered Inbound Transactions Covered Inbound Transaction Domestic acquiring corporation acquires all of the stock of the acquired CFC from a transferor CFC that, immediately before the transaction and any related transactions, owns (directly or indirectly under section 958(a)(2)) all of the stock of the acquired CFC, in one of the following transactions: Section 332 liquidation or upstream asset reorganization in which all of the stock of the transferor CFC is owned directly by the domestic acquiring corporation immediately before the transaction Other asset reorganization in which all of the stock of the transferor CFC is owned directly by a single domestic corporation (or members of the same consolidated group) and the same domestic corporation directly owns all of the stock of the domestic acquiring corporation immediately after the transaction and any related transactions Exception for de minimis stock ownership in transferor CFC ( 1 percent) 6

PTEP and Basis IRS Notice 2024-16 Limitations Limitations on the Scope of Covered Inbound Transactions De minimis boot. Boot is disqualifying, unless it is 1 percent of total FMV of stock of transferor CFC Loss in stock of acquired CFC. Transaction is not a covered inbound transaction if, immediately before the inbound transaction, the total amount of the transferor CFC s basis in the stock of the acquired CFC (including section 961(c) basis) exceeds the total FMV of such stock Drop downs. Transaction is not a covered inbound transaction if stock of the acquired CFC is transferred pursuant to section 368(a)(2)(C) or 1.368-2(k)(1), unless the transferee is (i) a member of the same consolidated group that includes the domestic acquiring corporation and wholly owned by members of the consolidated group, or (ii) the common parent of that consolidated group Other subsequent transfers. Transaction is not a covered inbound transaction if stock of the acquired CFC is transferred to a partnership or foreign corporation pursuant to a plan in connection with the inbound transaction (plan deemed to exist within 2-year period) RIC, REIT, S Corp. Does not apply if the domestic acquiring corporation is one of these entities If stock of multiple acquired CFCs is transferred by a single transferor CFC, these limitations apply separately with respect to each acquired CFC 7

PTEP and Basis IRS Notice 2024-16 Foreign Currency A taxpayer that has maintained section 961(c) basis in a currency other than the US dollar must, before applying the rules in Notice 2024-16, translate section 961(c) basis into US dollars, under a reasonable method consistently applied to all acquired CFCs in any covered inbound transaction undertaken by one or more domestic acquiring corporations Must use exchange rate that reflects the original US dollar inclusion amounts of the US shareholder that gave rise to the section 961(c) basis, reduced as appropriate, including to take into account distributions of PTEP on such stock Distributions of PTEP are treated as reducing the section 961(c) basis as so translated by the US dollar basis of the PTEP 8

PLR 202339009 (Public Company F Reorganization) Transaction Steps: SHs Sell FSub to Resulting for Notes Step 1 Parent forms Resulting, owning nominal shares 3 Parent Step 2 Parent subscribes for additional Resulting shares for nominal consideration, instructing Resulting to issues shares to Parent s shareholders pro rata; nominal shares canceled FSub Resulting Step 3 Parent sells FSub to Resulting for notes (non- interest bearing, demand) 1 Resulting Formation Step 4 Shareholders exchange Parent stock for Resulting stock Share-for-Share Exchange SHs SHs 4 Step 5 Resulting shares begin trading Step 6 Parent files notice to convert under local law to private limited company (eligible entity); a days after the share-for-share exchange, Parent converts Resulting Parent Resulting Notes Resulting Notes Parent Step 7 Effective on conversion date, Parent checks the box and becomes disregarded FSub Resulting 6 7 Parent Converts and Checks-the- Box FSub 10

PLR 202339009 (Public Company F Reorganization), cont d Representations: Step 3 is structured as a sale solely for local country purposes No planned purchase or sale of Resulting stock between Step 4 and Step 7 will be included in the plan of reorganization SHs Rulings: Steps 2, 3, 4, 6 and 7 will be treated as if 100% of Parent was contributed to Resulting and thereafter Parent made a check-the-box election Resulting Resulting Notes Period of time between Step 4 and Step 7 will not prevent section 368(a)(1)(F) qualification Sales or exchanges of Resulting stock during the period between Step 4 and Step 7 will not prevent section 368(a)(1)(F) qualification Issues/Questions: Treas. Reg. 1.368-2(m)(1)(ii): The same person or persons must own all of the stock of the transferor corporation, determined immediately before the potential F reorganization, and of the resulting corporation, determined immediately after the potential F reorganization, in identical proportions. However, this requirement is not violated if one or more holders of stock in the transferor corporation exchange stock in the transferor corporation for stock of equivalent value in the resulting corporation, but having different terms from those of the stock in the transferor corporation, or receive a distribution of money or other property from either the transferor corporation or the resulting corporation, whether or not in exchange for stock in the transferor corporation or the resulting corporation. How significant is the number of days at issue in Step 6 (to effectuate the local country conversion)? What is the meaning of the second representation that purchases/sales of Resulting stock will not be included in the plan of reorganization ? Parent FSub 11

OVERVIEW OF FACTS OVERVIEW OF FACTS Simplified Steps FP 1. Belgium DRE converted into a per se corporation w/ debt and NQPS outstanding (2) Upstream Sale of CFC 2 2. CFC 1 sold CFC 2 upstream to Foreign Parent USP Intended U.S. Tax Treatment Taxable contribution of Belgium assets to new Belgium CFC under section 351(b), triggering E&P for CFC 2 CFC1 E&P not taxed as GILTI, because CFC 2 continued to be a CFC due to the repeal of section 958(b)(4), but had no direct/indirect U.S. SH on last day of its year 13 CFC2 CFC 1 s gain on the sale of CFC 2 triggers section 964(e) dividend to USP, sourced to untaxed E&P CS, NQPS and Debt Section 964(e) dividend is not Subpart F income by reason of section 245A DRD Belgium NV/SA Belg. BVBA (1) Conversion into a Per Se Corp

PROCEDURAL POSTURE PROCEDURAL POSTURE Extraordinary reduction rules (Reg. 1.245A-5(e)) deny a section 245A DRD for this type of transaction. But regulations were retroactive and issued on a temporary basis w/o notice and comment. Colorado District Ct concluded lack of notice and comment violated the APA, rejecting the Government s argument that it needed to rush the regulations to prevent abuse. IRS then pivots to economic substance arguments IRS attempting to disregard the taxable incorporation transaction (conversion to per se entity), so as to disregard the resulting E&P, which would convert the stock gain into Sub F income No business purpose/economic significance for the conversion into a per se corporation (along with issuance of NQPS and notes) Step transaction argument that existence of per se Belgian corporation was transitory 14 1 4

DISTRICT COURT HOLDS FOR GOVERNMENT DISTRICT COURT HOLDS FOR GOVERNMENT Section 7701(o) - In the case of any transaction in which the economic substance doctrine is relevant The determination of whether the economic substance doctrine is relevant to a transaction shall be made in the same manner as if [section 7701(o)] had never been enacted. Relevance Inquiry Rejected Relevance Inquiry Rejected [T]here is no threshold relevance inquiry that precedes the inquiry into a transaction s economic substance. Instead, the doctrine s relevance is coextensive with the statute s test for economic substance. The question of whether the [transaction] lacks economic substance is equivalent to the question of whether the tax benefits achieved in the transaction violate congressional intent and is analyzed using the enumerated statutory prongs, i.e., (1) no meaningful change to non-tax economic position, and (2) no substantial purpose apart from tax effects. 15 No Exemption Available to No Exemption Available to LGI LGI LGI s transaction was not a basic business transaction. [A] series of transactions that constitute a corporate organization or reorganization might fall outside the economic substance doctrine, but a series of transactions that merely includes a reorganization is not necessarily exempt. 1 5

DISTRICT DISTRICT COURT HOLDS FOR GOVERNMENT COURT HOLDS FOR GOVERNMENT Unit of Analysis Unit of Analysis The proper unit of analysis is the transaction in aggregate. Court refused to analyze any step or phase in isolation, even if it could be said that the tax benefit at issue was created because of a particular step. Applying the Section 7701(o) Prongs Applying the Section 7701(o) Prongs Prong 1: No Meaningful Change to LGI s Economic Position 16 LGI conceded that three of the four steps in the transaction did not change its economic position in a meaningful way. Court: That concession controls. Non-tax economic consequences, if not meaningful, are insufficient. Prong 2: No Substantial Non-Tax Purpose LGI claimed the transaction was in furtherance of Belgian corporate law requirements. Court: LGI failed to sufficiently indicate how the transaction facilitated such compliance. Court: A transaction may be in furtherance of some end without being a substantial purpose. [T]he only substantial purpose of the transaction was tax evasion. 1 6

Proposed Section 367(b) Regulations Treasury and the IRS on October 5 issued proposed regulations (Proposed Regulations) (REG- 117614-14) providing guidance on the taxation of cross-border triangular reorganizations and related transactions. The Proposed Regulations modify regulations previously announced in Notice 2014-32 and Notice 2016-73. Notice 2014-32 addressed transactions that Treasury viewed as exploiting certain aspects of final regulations published on May 19, 2011 under Section 367(b) (the 2011 Final Regulations). Notice 2016-73 contained additional rules to address transactions that Treasury viewed as exploiting the 2011 Final Regulations, as modified by the rules announced in Notice 2014-32, and announced that additional regulations would be issued under Section 367. With respect to the rules described in Notice 2014-32, the Proposed Regulations generally would apply to transactions completed on or after April 25, 2014, subject to limited exceptions. For the rules described in Notice 2016-73, the Proposed Regulations generally would apply to transactions completed on or after December 2, 2016. To the extent the Proposed Regulations contain rules not previously announced in Notice 2016-73, the Proposed Regulations would be applicable to transactions completed on or after December 6, 2023, the date the Proposed Regulations are filed in the Federal Register. Comments were due by December 5, 2023. 18

Prop. Treas. Reg. 1.367(b)-3(g)(6), Example 1 Inbound F Reorganization with Excess Asset Basis Facts Analysis Analysis: : The F Reorganization is an asset acquisition described in section 368(a)(1) and is thus subject to section 367(b) and Prop. Treas. Reg. 1.367(b)-3(g). Under Prop. Treas. Reg. 1.367(b)-3(b)(3), USP and USS each must include in income as a deemed dividend the all E&P amount with respect to their stock of FP. Because there is excess asset basis ( EAB determined in Prop. Treas. Reg. 1.367(b)-3(g)(6)(i)(B)(2)), USP and USS must compute the all E&P amounts attributable to their stock of FP as if FP had received a distribution of specified earnings, immediately before the F reorganization. Because the stock of FS2 is indirectly owned by FP, to the extent the specified earnings are determined by reference to the E&P of FS2, FS2 is treated as making a distribution to FS1 under section 301, and FS1 is then treated as making a distribution to FP under section 301 in an amount equal to the sum of the amount of specified earnings determined by reference to the E&P of FS1 (determined without regard to the deemed distribution from FS2) and the amount of the deemed distribution received from FS2. EAB The amount of FP s EAB is $50x, calculated as the amount by which FP s inside asset basis ($95x) exceeds: (i) the sum of FP s E&P ($40x), (ii) the aggregate basis in the outstanding stock of FP ($5x), and (iii) the amount of liabilities of FP assumed by US Newco in the F Reorganization ($0). A. USP EAB ) with respect to FP (as 80% FMV = $80x AB = $4x E&P = $32x 20% FMV = $20x AB = $1x E&P = $8x USS US Newco stock 2 Assets AB = $95x Liabilities = $0 E&P = $40x 2 US Newco stock FP 1 Transfer all FP s assets B. US Newco stock 1 FS1 US Newco E&P = $30x FS2 E&P = $70x 19

Prop. Treas. Reg. 1.367(b)-3(g)(6), Example 1 (continued) Inbound F Reorganization with Excess Asset Basis Analysis Analysis Analysis(continued) (continued): : Deemed Distribution of Specified Earnings The amount of specified earnings equals $50x, the lesser of the following amounts: (i) $100x, the sum of the E&P of FS1 and FS2; and (ii) $50x, the amount of EAB with respect to FP. Accordingly, FP is treated as receiving a distribution of $50 from FS1. Under Prop. Treas. Reg. 1.367(b)-3(g)(3), $15x ($50x x ($30x / $100x)) of FS1 s E&P and $35x ($50x x ($70x / $100x)) of FS2 s E&P are designated as specified earnings. FS2 is treated as distributing $35x to FS1. Under sections 301(c)(1) and 954(c)(6), the $35x deemed distribution from FS2 to FS1 is treated as a dividend that does not give rise to FPHCI. FS1 must accordingly increase its E&P described in section 959(c)(3) by $35x to $65x, and FS2 must decrease its E&P described in section 959(c)(3) by the same amount. FS1 is then treated as making a distribution of $50x to FP. Under sections 301(c)(1) and 954(c)(6), the $50x deemed distribution is also treated as a dividend that does not give rise to FPHCI. FP must accordingly increase its E&P described in section 959(c)(3) by $50x to $90x, and FS1 must decrease its E&P described in section 959(c)(3) by the same amount. C. USP 80% USS FMV = $80x AB = $4x E&P = $32x + $40x = $72x 20% FMV = $20x AB = $1x E&P = $8x + $10x = $18x Assets AB = $95x Liabilities = $0 FP E&P = $40x + $50x = $90x Deemed Distribution of $50x E&P = $30x +$35x - $50x = $15x FS1 Deemed Distribution of $35x E&P = $70x - $35x = $35x FS2 20

Prop. Treas. Reg. 1.367(b)-3(g)(6), Example 1 (continued) Inbound F Reorganization with Excess Asset Basis Analysis Analysis Analysis(continued) (continued): : Adjusted all E&P amount attributable to USP s FP stock Under Prop. Treas. Reg. 1.367(b)-3(g)(1), USP must compute the all E&P amount attributable to its stock of FP after taking into account the $50x increase to FP s E&P that resulted from the deemed distribution of specified earnings. Because USP owns 80% of the stock of FP, $40x (calculated as 80% of $50x) of the specified earnings are attributable to USP s stock of FP and are included in the all E&P amount attributable to USP s stock of FP. The all E&P amount that USP must include in income as a deemed dividend is therefore $72x ($32x + $40x). Adjusted all E&P amount attributable to USS s FP stock. Under Prop. Treas. Reg. 1.367(b)-3(g)(1), USS must compute the all E&P amount attributable to its stock of FP after taking into account the $50x increase to FP s E&P that resulted from the deemed distribution of specified earnings. Because USS owns 20% of the stock of FP, $10x (calculated as 20% of $50x) of the specified earnings are attributable to USS s stock of FP and are included in the all E&P amount attributable to USS s stock of FP. The all E&P amount that USS must include in income as a deemed divided is therefore $18x ($8x + $10x). D. USP 80% USS FMV = $80x AB = $4x E&P = $32x + $40x = $72x 20% FMV = $20x AB = $1x E&P = $8x + $10x = $18x E. Assets AB = $95x Liabilities = $0 FP E&P = $40x + $50x = $90x Deemed Distribution of $50x E&P = $30x +$35x - $50x = $15x FS1 Deemed Distribution of $35x E&P = $70x - $35x = $35x FS2 21

Prop. Treas. Reg. 1.367(b)-3(g)(6)(ii), Example 2 Section 332 Liquidation of a First-Tier CFC with Excess Asset Basis Facts Analysis A. All E&P Amount: USP 1) The FP Liquidation is subject to section 367(b) and Prop. Treas. Reg. 1.367(b)-3. Under Prop. Treas. Reg. 1.367(b)-3(b)(3), USP must include in income as a deemed dividend the all E&P amount with respect to its FP stock. All E&P = $50x 1 FP Liquidation 2) Because there is EAB with respect to FP, USP must compute the all E&P amount attributable to its FP stock as if FP had received a distribution of specified earnings immediately before the FP Liquidation. EAB = $100x E&P = $50x FP B. Deemed distribution of specified earnings: 1) The amount of specified earnings equals $100x, the lesser of the following amounts: (i) $200x, the E&P of FS; and (ii) $100x, the amount of EAB with respect to FP. PTEP = $200x 2) FS is accordingly treated as making a distribution of $100x to FP. FS i. Under sections 301(c)(1) and 959(b), the $100x deemed distribution from FS to FP is treated as a distribution of PTEP that is not included in the gross income of FP for purposes of section 951. ii. The distribution reduces FS s E&P and PTEP with respect to USP by $100x and increases FP s E&P and PTEP with respect to USP by $100x. iii. Appropriate adjustments are made under section 961 for the distribution of PTEP. 22

Prop. Treas. Reg. 1.367(b)-3(g)(6)(ii), Example 2 Section 332 Liquidation of a First-Tier CFC with Excess Asset Basis Analysis Analysis Income = $50x USP C. Adjusted All E&P attributable to USP s stock of FP: 1) Under Prop. Treas. Reg. 1.367(b)-3(g)(1), USP must compute the all E&P amount attributable to its FP stock after taking into account the $100x increase to FP s E&P that resulted from the deemed distribution of specified earnings. 2) Because the deemed distribution consisted entirely of PTEP with respect to USP, the deemed distribution does not affect USP s all E&P amount of $50x. See Treas. Reg. 1.367(b)-2(d)(2)(ii). 3) USP must therefore include $50x in income as a deemed dividend under Prop. Treas. Reg. 1.367(b)-3. USP must also recognize any foreign currency gain or loss under section 986(c) with respect to the $100x of PTEP of FP. See Treas. Reg. 1.367(b)-2(j)(2). All E&P = $50x + $0 = Deemed distribution of specified earnings of $100x $50x EAB = $100x E&P = $50x PTEP = $100x FP Deemed distribution of $100x of PTEP PTEP = $200x - $100x = $100x FS 23

Prop. Treas. Reg. 1.367(b)-4(g)(3), Example Facts Analysis Analysis: : USP Reg. . 1 1. .367 (A) (A)Application Applicationof of Treas The triangular B reorganization is described in Treas. Reg. 1.367(b)-10, and the $60 of cash constitutes property under Treas. Reg. 1.367(b)-10(a)(3)(ii). Pursuant to Treas. Reg. 1.367(b)-10(b)(1), adjustments must be made that have the effect of a distribution of property in the amount of $60x from FS to FP under section 301. The $60x deemed distribution is treated as separate from, and occurring immediately before, FS s acquisition of the 60% FP block used in the triangular B reorganization. The $60x deemed distribution from FS to FP results in $60x of dividend income to FP under section 301(c)(1) that is not FPHCI under section 954(c)(6). Reg. . 1 1. .367 367(b) (b)- -4 4(g) Pursuant to Treas. Reg. 1.367(a)-3(a)(2)(iv)(B), Prop. Treas. Reg. 1.367(b)- 4(g) applies to $60x of the stock of FT (the 60% FT block) exchanged for the 60% FP block. Thus, under Prop. Treas. Reg. 1.367(b)-4(g)(1)(i), USS must include in income a $30x deemed dividend (representing 60 percent of USS s $50x section 1248 amount) with respect to the 60% FT block exchanged for the 60% FP block. Treas. .Reg 367(b) (b)- -10 10: : USS $40 of FS stock $60 of cash 1 2 FP Transfers $100 FP Voting Stock Issues $100 FP Voting Stock 1 (B) (B)Application Applicationof of Prop Prop. .Treas Treas. .Reg (g): : FS E&P: $60 FMV: $100 Adjusted Basis: $20 1248 Amount: $50 FT 24

Prop. Treas. Reg. 1.367(b)-4(g)(3), Example Analysis Analysis Analysis(Continued) (Continued) Reg. . 1 1. .367 (C) (C)Application Applicationof of Prop In addition, under Prop. Treas. Reg. 1.367(b)-4(g)(1)(ii), USS must recognize its realized gain that would not otherwise be recognized with respect to the 60% FT block. USS s FMV and adjusted basis in the 60% FT block are $60x (60 percent of the $100x FMV of the stock of FT) and $12x (60 percent of the $20x adjusted basis of the stock of FT), respectively. USS s initial built-in gain with respect to the 60% FT block is accordingly $48x ($60x FMV less $12x adjusted basis). The $30x deemed dividend increases USS s basis in the 60% FT block to $42 ($12x + $30x), leaving $18x ($60x - $42x) of built-in gain. Prop. .Treas Treas. .Reg 367(b) (b)- -4 4(g) (g)cont cont.: .: USP USS Deemed dividend of $60x Deemed dividend = ($50x x 60%)= $30x A BIG in 60% FT stock FMV = $100x x 60% = $60 AB = $20x x 60% = $12 Initial BIG = $60 - $12 = $48 AB is increased by $30x of the deemed dividend income BIG = $48 - $30 = $18 B FP o USS must therefore recognize the remaining $18x of gain with respect to the 60% FT block. (D) (D)Application Applicationof of Prop USS has $32x of built-in gain in the remaining $40x of stock of FT (the 40% FT block) that USS exchanged for the 40% FP block, calculated as USS s initial $80 of built-in gain in all of its stock of FT less the $48x of initial built-in gain attributable to the 60% FT block. USS s section 1248 amount in the 40% FT block is $20x, calculated as 40 percent of USS s $50x section 1248 amount. USS does not recognize a deemed dividend of the $20x section 1248 amount under Prop. Treas. Reg. 1.367(b)-4(b) because FT remains a controlled foreign corporation with respect to which USS is a section 1248 shareholder immediately after the triangular B reorganization. Unless USS properly files a gain recognition agreement pursuant to Treas. Regs. 1.367(a)-3(b) and 1.367(a)-8, USS recognizes the $32x of built-in gain under section 367(a)(1) with respect to the 40% FT block. Prop. .Treas Treas. .Reg Reg. . 1 1. .367 367(b) (b)- -4 4(b) (b)and andregulations regulationsunder undersection section367 367(a) (a) C FS BIG in 40% FT stock BIG = ($100x - $20x) - $48 = $32 1248 amount in the 40% FP block = $50x x 40% = $20x E&P = $60x -60x = $0x FT FMV: $100 Adjusted Basis: $20 1248 Amount: $50 25

Prop. Treas. Reg. 1.367(b)-10(d)(2), Example 1 Anti-Abuse Rule: Deemed increase to S s E&P Facts Analysis Analysis: : Because USS s purchase of the $90x of stock of FP in exchange for the USS note is engaged in with a view to avoid the purpose of Prop. Treas. Reg. 1.367(b)-10, the anti-abuse rule applies and appropriate adjustments are made. In particular, for purposes of determining the consequences of the deemed distribution provided for in Prop. Treas. Reg. 1.367(b)- 10(b)(1), the E&P of USS are deemed to include the E&P of UST. USS is therefore treated as having made a deemed distribution equal to $90x, which reflects the portion of the stock of FP that USS acquired in exchange for property (the USS Note). Because USS is deemed to have $100x of E&P, the entire $90x deemed distribution is treated as a dividend under section 301(c)(1). The deemed distribution is treated as separate from, and occurring immediately before, USS s acquisition of the stock of FP used in the triangular B reorganization. No adjustments are made by FP to the basis in its stock of USS except as provided in Treas. Reg. 1.358-6. Under Prop. Treas. Reg. 1.367(b)-10(b)(3), FP s adjustment to the basis in its stock of USS under Treas. Reg. 1.358-6 is determined as if FP provided all $100x of the stock of FP pursuant to the plan of reorganization. A. Deemed distribution of $90x FP + B. FP stock $90x USS note $90x USS stock $10x FP stock $10x 2.1 2.2 - USS E&P: $0 C. D. Foreign Person FP + FP stock $100x 4 UST stock USS UST - E&P: $100x E&P: $0 UST E&P: $100x 26

Prop. Treas. Reg. 1.367(b)-10(d)(3), Example 2 Anti-Abuse Rule: Downstream Property Transfer Analysis Analysis: A. Because FS1 s transfer of the USP Note to USS Newco is in connection with a triangular reorganization and is engaged in with a view to avoid the purpose of Prop. Treas. Reg. 1.367(b)-10, the anti-abuse rule of Prop. Treas. Reg. 1.367(b)-10(d) applies and the following adjustments are made: 1) FS1 s formation of USS Newco and transfer of the USP Note to USS Newco, together with the distribution of the shares of USS Newco pursuant to the liquidation of FS1, is treated under the anti-abuse rule as a distribution of $100x, consistent with its substance. Accordingly, the following adjustments are made consistent with such distribution: i. Because FS1 has more than $100x of E&P, the adjustments made are consistent with USS Newco having received a $100x dividend from FS1 separate from, and immediately before, the Triangular C Reorganization. USS Newco must therefore include $100x in gross income as if it had received that amount as a dividend and increase its E&P by the same amount. FS1 must decrease its E&P by $100x. ii. For purposes of determining USS Newco s basis in its stock of FS2 Newco, Treas. Reg. 1.367(b)-13 applies by treating USS Newco as P (within the meaning of Treas. Reg. 1.367(b)-13(a)(2)(ii)). Under Prop. Treas. Reg. 1.367(b)- 10(b)(3), USS Newco s adjustment to the basis in its FS2 Newco stock under Treas. Reg. 1.367(b)-13 is determined as if USS Newco provided the stock of USS Newco stock pursuant to the plan of reorganization. USP - Liquidating distribution 3 USP Note + FS1 Decrease E&P $100x E&P Deemed distribution of $100x USP Note 1 USS Newco + Income: $100x $100x of E&P No E&P 2 All FS1 assets (other than USS Newco stock) for USS Newco stock FS2 Newco 27

Prop. Treas. Reg. 1.367(b)-10(d)(4), Example 3 Anti-Abuse Rule: Taxable Debt Exchange Facts Analysis: A. Because the transfers of the FS Note are in connection with a triangular reorganization and are engaged in with a view to avoid the purpose of Prop. Treas. Reg. 1.367(b)-10, the anti-abuse rule of Prop. Treas. Reg. 1.367(b)-10(d) applies and the following adjustments are made: 1) FS is treated as having made a distribution to FP of $100x, reflecting the value of the FP stock that FS acquired for the FS Note. This deemed distribution is treated as separate from, and occurring immediately before, FS s acquisition of the FP stock used in the Triangular B Reorganization. i. Because FS has more than $100x of E&P, the entire deemed distribution is treated as a dividend under section 301(c)(1). ii. The deemed dividend causes FP to increase its E&P by $100x but does not constitute FPHCI to FP under section 954(c)(6). Thus, FP has $100x of E&P available to support inclusions under section 951(a)(1)(B) in connection with FP s subsequent acquisition of the USP Note. iii. No adjustments are made by FP to the basis in its FS stock except as provided in Treas. Reg. 1.358-6. Under Prop. Treas. Reg. 1.367(b)-10(b)(3), FP s adjustment to the basis in its FS stock under Treas. Reg. 1.358-6 is determined as if FP provided the FP stock pursuant to the plan of reorganization. - 3 3 USP USP Note ($100x FMV) FS Note for USP Note + FS Note ($100x FMV) $100x of FP voting stock E&P = $0 + $100x = $100x FP USS FS Note $100x of FP voting stock 1 1 $100x deemed distribution 2 - FS UST UST stock Decrease E&P $100x UST 28

Section 367(d) Proposed Regulations for Repatriation of IP On May 2, 2023, Treasury and the IRS released proposed rules that would terminate the continued application of section 367(d) arising from a prior outbound transfer of intangible property (IP), when the IP is repatriated to certain qualified U.S. persons. Continued application of section 367(d) in these situations could result in excessive U.S. taxation and may disincentivize certain repatriations of intangible property. Section 367(d) generally treats an outbound transfer of IP as a sale for contingent payments, and requires the U.S. transferor to include amounts annually over the life of the IP The proposed rules provide a mechanism to terminate this annual inclusion when the IP is repatriated and would apply to repatriation of IP occurring on or after publication of final regulations. 30

Section 367(d) Proposed Regulations for Repatriation of IP Sec. 367(d) termination occurs if (i) the IP is transferred by the foreign corporation to a Qualified Domestic Person (generally, the U.S. transferor, related U.S. person, or successor) and (ii) reporting requirements are met Tax consequences to U.S. transferor. The U.S. transferor includes in income a final partial annual inclusion, and depending on the form of the transaction, must recognize gain Foreign corporation adjustments. The E&P and gross income of the foreign corporation are reduced to offset the impact of the gain shifted to the U.S. transferor. Qualified domestic person s adjusted basis in the repatriated IP. If the IP is NOT transferred basis property, the adjusted basis is equal to the FMV of the IP If the IP is transferred basis property, the adjusted basis is The lesser of the U.S. transferor s former adjusted basis in the IP or the transferee foreign corporation s adjusted basis in the IP, increased by The greater of the gain recognized by the U.S. transferor or the foreign corporation 31

Section 367(d) Proposed Regulations for Repatriation of IP (Examples) 32 32

Cross-Border M&A Tax: Increasing Complexity Significantly increased complexity with enactment of TCJA in 2017 GILTI FDII BEAT And now again starting in 2023 CAMT Effective January 1, 2023 GloBE EU members formally adopted directive on December 15, 2022 IIR effective as of January 1, 2024 UTPR effective as of January 1, 2025 UTPR safe harbor for first two years if ultimate parent entity jurisdiction has corporate income tax rate of at least 20% Certain transition rules apply to intragroup transactions occurring after November 30, 2021 34

Evaluating Cross-Border Transactions Under Multiple Regimes Modeling is already imperative post-TCJA; now, taxpayers will need to model results under all three regimes Results will not be intuitive and, initially, perhaps also unfamiliar to M&A tax practitioners who are not well versed in financial accounting There are meaningful differences between the three regimes US federal income tax A standalone system, differs from financial accounting In particular, structure of transaction stock vs. asset sale, tax-free vs. taxable matters CAMT and GloBE start with financial accounting principles GAAP Structure of transaction often doesn t matter E.g., in consolidation, all departures from group generally trigger gain based on asset carrying value Buyer group generally steps up asset carrying value to FMV 35

Evaluating Cross-Border Transactions Under Multiple Regimes (cont d) IFRS Broadly speaking comparable to GAAP, but there are differences E.g., push down of purchase accounting adjustments CAMT and GloBE both contain adjustments to the baseline financial accounting rules Under CAMT: Treatment of tax consolidated group Special rules for inclusions with respect to non-consolidated subsidiaries Dividends and other includible or deductible amounts under the Code (other than GILTI and Subpart F) Inclusion of pro rata share of CFC AFSI Under GloBE: Effectively ignores purchase and pushdown accounting adjustments Ignores equity method, most dividends, and gains/losses from dispositions of equity interests (unless Equity Investment Inclusion Election or <10% portfolio holding) 36

Evaluating Cross-Border Transactions Under Multiple Regimes (cont d) Every transaction will need to be evaluated and modeled from all three perspectives, both to determine the specific consequences of the transaction, as well as whether the disposition or acquisition will get you the taxpayer into or out of CAMT or GloBE in the first place CAMT Threshold Average annual AFSI for three-year period exceeds $1 billion For foreign-parented MNE, $1 billion threshold and its US entities (including foreign entities effectively connected income) together have average annual AFSI for three-year period exceeding $100 million Notice 2023-7 provides rules for acquisitions, dispositions and corporate separations GloBE Threshold More than 750 million in annual global revenue for two of prior four fiscal years Special rules for mergers, demergers, and constituent entities joining or leaving a group 37

Buy Side: Example 1 (No Foreign Tax or GW) Foreign Co Public Public US Buyer US Buyer $500 Foreign Co Foreign Co Tax rate = 0% FMV = $100 Tax Basis = $0 Book CV = $0 Useful life = 10 years FMV = $400 Tax Basis = $0 Book CV = $0 Useful life = 10 years Foreign Foreign Intangibles Intangibles (not goodwill) (not goodwill) Foreign Foreign Tangibles Tangibles Facts and assumptions Facts and assumptions US Buyer agrees to purchase the stock of Foreign Co from its shareholders for $500, and wants to determine the benefit to it (if any) of making a Section 338(g) election for the purchase. US Buyer US Buyer Applicable corporation for CAMT purposes Owns at least one CFC incorporated in a jurisdiction that has adopted a UTPR (not depicted) Prepares financial statements under US GAAP 15% ETR from legacy operations Foreign Co Foreign Co Resident in jurisdiction with 0% tax rate Owns two kinds of assets foreign tangible assets and foreign intangible assets other than goodwill all of which have a useful life of 10 years for book and tax purposes Expected to generate $200 of income (excluding depreciation) for book and tax purposes in the year after purchase 38

CAMT Adjustments to AFSI for Depreciation Section 56A(c)(13): Adjust AFSI for depreciation deductions allowed under Section 167 with respect to Section 168 property. Notice 2023-7: Depreciation adjustments necessary to reduce AFSI by tax depreciation expense and to disregard depreciation expense reflected on the AFS. Tax depreciation adjustment includes amounts that have been: Capitalized and recovered as COGS in computing taxable income for the tax year, and Allowed as a deduction in computing taxable income for the tax year. AFSI adjusted to disregard: Depreciation expense and impairment loss / reversal included in COGS in the AFS, Depreciation expense and impairment loss / reversal taken into account in the AFS, and Amounts recognized as an expense or loss in the AFS and as depreciable basis for tax purposes. Applicability - depreciation adjustments set forth in the Notice apply to property placed in service in any taxable year 39

CAMT Inclusion of CFC income Section 56A(c)(3): US Shareholder of a CFC includes pro rata share of items that are taken into account in computing the net income or loss set forth on the CFC s AFS. CFC net loss does not reduce U.S. Shareholder s AFSI but can be carried forward to succeeding taxable year Not taken into account for CAMT purposes Section 250 deductions Section 245A dividends-received deductions QBAI Exempt income (e.g., foreign oil and gas income) 40

Purchase Accounting: In General Under both US GAAP and IFRS, an acquisition of target equity in a change of control transaction (as well as an acquisition of assets representing a business) is reflected as an acquisition of the target s assets on the consolidated financial statements of the MNE group. Under this so-called purchase accounting, the assets of the target entity are recorded on the consolidated financial statements of the MNE group at FMV and goodwill (or a bargain purchase) is recognized. 41

Push Down Accounting Under push down accounting, assets are not only stepped up (or down) to FMV at the target entity level but are also stepped up (or down) with respect to all of the target s direct and indirect controlled subsidiaries where the purchase price adjustments are recognized in the stand-alone financial statements of the target. Under U.S. GAAP (ASC 805), after the acquisition, the target generally has the option to apply push down accounting in its separate financial statements. Under IFRS (IFRS 3), push down accounting is not permitted. 42

Purchase Accounting under GloBE Buyer Consequences Art. 6.2.1(c) in the acquisition year and each succeeding year, the target shall determine its GloBE Income or Loss and Adjusted Covered Taxes using its historical carrying value of the assets and liabilities Seller Buyer Commentary to Art. 6.2.1 ( 51) Where the financial accounting standard permit the UPE to push down adjustments to the carrying value of assets and liabilities that were attributable to a purchase of a business to the separate accounts of the acquired Constituent Entity, the Constituent Entity may use the carrying value reflected in its separate accounts if the acquisition occurred prior to 1 December 2021 and the MNE Group does not have sufficient records to determine its Financial Accounting Net Income or Loss with reasonable accuracy based on the adjusted carrying values of the acquired assets and liabilities. Sale Target Target Seller Consequences Art. 3.2.1(c) Globe Income or Loss does not include Excluded Equity Gain or Loss Art. 10.1 Excluded Equity Gain or Loss includes gains and losses from disposition of an Ownership Interest, except for a disposition of a Portfolio Shareholding Art. 4.1.3(a) Covered Taxes do not include current tax expense with respect to income excluded from the computation of GloBE Income or Loss under Chapter 3 43

Allocation of CFC taxes under GloBE Article 4.3.2(c) of the GloBE Rules require the allocation of some CFC taxes from the Constituent Entity-Owner that is subject to a CFC regime to the CFC that gave rise to the CFC charge. A specific methodology is not prescribed and the Commentary states that CFC taxes should be allocated based upon a Constituent Entity s share of the underlying income. Administrative guidance clarifies how CFC taxes should be allocated when such taxes are generated under a 'Blended CFC Tax Regime', which is a CFC tax that is computed based on a blend of income, losses and / or creditable taxes of multiple CFCs whose ownership interests are held by a constituent entity-owner (or multiple constituent entity-owners that file a single tax return) . Confirms that GILTI, in its current form, meets the definition of a CFC Tax Regime. GILTI is an example of a Blended CFC Tax Regime, the guidance outlines an agreed simplified allocation that can be applied to Blended CFC Tax Regimes, including GILTI, for a limited time period. GILTI tax is only allocated to low-taxed constituent entities (i.e., ETR < 13.125%) If no such entities exist in the group, tax remains in the U.S. group Subpart F and CAMT are not expected to be Blended CFC Tax Regimes. 44

Buy Side: Example 1 (contd) US Buyer Foreign Co Tax rate = 0% Foreign Intangibles (not goodwill) Foreign Tangibles Book US FIT Year 1 results: No 338 338 Income (ex depreciation) 200 200 200 Depreciation - tangibles (10) - (10) Depreciation - intangibles Net income (40) 150 - (40) 150 200 * Assumes that tangible assets are depreciated under 168, so Foreign Co uses tax depreciation ($0) w/r/t such assets when computing AFSI ** Because the top-up tax is imposed under the UTPR, assumes GloBE tax is not creditable for U.S. tax or CAMT purposes Note that calculations reflect rounding 45

Buy Side: Example 1 (contd) GILTI Without a 338 election, US Buyer has no basis in the Foreign Co assets, so no depreciation or deductions for QBAI Section 338 election gives US Buyer a stepped up basis in Foreign Co s assets, which allows it to take: $50 of depreciation/amortization deductions A deduction for 10% of its QBAI (i.e., its tangible assets) CAMT 338 election largely does not affect CAMT because book-based; instead, GAAP purchase accounting rules give US Buyer FMV carrying value in Foreign Co s assets Except under CAMT, tangible assets are still depreciated using 168 tax depreciation without 338 election, no stepped up basis, so no depreciation of tangible assets CAMT eliminates benefit of GILTI rate and deduction for QBAI GloBE CAMT and GloBE are both based on book accounting But no purchase accounting adjustments under GloBE (unlike CAMT) assets are acquired with carryover book carrying value (i.e., $0), so no depreciation deductions Therefore, even though CAMT and GloBE apply the same minimum tax rate of 15%, because no purchase accounting in GloBE, a top-up tax is owed under GloBE on top of the CAMT liability * Assumes that tangible assets are depreciated under 168, so Foreign Co uses tax depreciation ($0) w/r/t such assets when computing AFSI ** Because the top-up tax is imposed under the UTPR, assumes GloBE tax is not creditable for U.S. tax or CAMT purposes Note that calculations reflect rounding 46

Buy Side: Example 2 (Foreign Tax and GW) Foreign Co Public US Buyer $500 Foreign Co Tax rate = 5% Foreign Intangibles (not goodwill) Foreign Goodwill FMV = $200 Tax Basis = $0 Book CV = $0 Useful life = 10 years FMV = $300 Tax Basis = $0 Book CV = $0 Facts and assumptions The facts and assumptions are the same as Example 1, except that: Foreign Co is resident in a jurisdiction with a 5% tax rate Foreign Co owns two kinds of assets foreign intangibles with a useful life of 10 years and foreign goodwill

Foreign Tax Credits under CAMT Section 59(l) provides for a CAMT FTC for: A foreign income tax within the meaning of section 901 That is taken into account on the applicable financial statement of the applicable corporation or its CFC And is paid or accrued (for Federal income tax purposes) by the applicable corporation or the CFC 15% limitation on foreign income taxes paid or accrued by a CFC, with a 5-year carryforward of CFC foreign taxes It appears that neither section 901(m) nor section 904 limitations should apply for purposes of the CAMT FTC. 48

Buy Side: Example 2 (contd) US FIT / GILTI No 338 338 21.0% Net CFC tested income NDTIR (10% of QBAI) GILTI Taxes disallowed under Sec. 901(m) Sec. 78 gross-up Sec. 250 deduction (50% of GILTI + Sec. 78 gross-up) GILTI inclusion Corporate income tax rate Pre-FTC tax on GILTI Indirect FTC (80% of foreign income taxes) GILTI tax liability 190 150 US Buyer US Buyer - - 190 150 (2) 8 (79) 79 21.0% 10 Tax rate = 5% (Tax = $10) (100) 100 Foreign Co Foreign Co 21 (8) 13 17 (6) 10 Foreign Foreign Intangibles Intangibles (not goodwill) (not goodwill) Foreign Foreign Goodwill Goodwill CAMT No 338 338 AFSI CAMT rate 15% of AFSI CAMT FTC Tentative minimum tax Regular tax liability BEAT liability CAMT liability 180 15% 27 (10) 17 (13) 180 15% 27 (10) 17 (10) Book US FIT Year 1 results: No 338 338 Income (ex depreciation) Depreciation tangibles Depreciation non-GW intang. Depreciation GW Net income 200 200 200 - - - - - 4 7 (20) - - (20) (20) 160 GloBE No 338 338 - GLoBE Income Adjusted Covered Taxes (Local tax + GILTI tax + CAMT) GloBE ETR Top-up Tax Percentage (15% minus GloBE ETR) SBIE Excess Profit Top-up Tax 200 27 14% 2% 200 27 14% 2% 180 200 - - 200 200 * For simplicity, ignores deductibility of foreign taxes disallowed for credit purposes under 901(m). Also assumes that 901(m) does not apply for CAMT purposes ** Because the top-up tax is imposed under the UTPR, assumes GloBE tax is not creditable for U.S. tax or CAMT purposes Note that calculations reflect rounding 3 3 No 338 180 338 Total tax in first post-acquisition year Pre-tax book income Foreign Co ETR for book purposes 30 30 180 17% 17%

Buy Side: Example 2 (contd) US FIT / GILTI No 338 338 21.0% GILTI 338 election creates amortizable basis in assets ($40 deduction) Net CFC tested income NDTIR (10% of QBAI) GILTI Taxes disallowed under Sec. 901(m) Sec. 78 gross-up Sec. 250 deduction (50% of GILTI + Sec. 78 gross-up) GILTI inclusion Corporate income tax rate Pre-FTC tax on GILTI Indirect FTC (80% of foreign income taxes) GILTI tax liability 190 150 - - 190 150 (2) 8 (79) 79 21.0% 10 Addition of $10 of foreign taxes at Foreign Co means: Net CFC tested income is reduced by foreign taxes (but foreign taxes added back via 78 gross-up) FTC equal to only 80% of foreign income taxes In addition, with 338 election, becomes covered asset acquisition subject to 901(m) disallowance of 20% ($40 basis difference $200 tax base) CAMT Lose benefit of basis step-up with 338 election In addition to higher rate, no book depreciation on goodwill But GILTI rate cut-back is reduced because CAMT FTC is more favorable than regular tax FTC Not limited to 80% of foreign taxes paid and likely not subject to 901(m) disallowance GloBE No purchase accounting adjustments to carrying value of assets means no additional depreciation FTC also affects calculation Accordingly, GloBE top-up tax owed because of (1) no depreciation and (2) CAMT FTC, clawing back benefit of both that remained after application of CAMT (100) 100 21 (8) 13 17 (6) 10 CAMT No 338 338 AFSI CAMT rate 15% of AFSI CAMT FTC Tentative minimum tax Regular tax liability BEAT liability CAMT liability 180 15% 27 (10) 17 (13) 180 15% 27 (10) 17 (10) - - 4 7 GloBE No 338 338 GLoBE Income Adjusted Covered Taxes (Local tax + GILTI tax + CAMT) GloBE ETR Top-up Tax Percentage (15% minus GloBE ETR) SBIE Excess Profit Top-up Tax 200 27 14% 2% 200 27 14% 2% - - 200 200 3 3 No 338 180 338 Total tax in first post-acquisition year Pre-tax book income Foreign Co ETR for book purposes 30 30 180 17% 17% 50

")

")

,")

Regulations")

Regulations")

-3(g)(6), Example 1")

-3(g)(6), Example 1 (continued)")

-3(g)(6), Example 1 (continued)")

-3(g)(6)(ii), Example 2")

-3(g)(6)(ii), Example 2")

-4(g)(3), Example")

-4(g)(3), Example")

-10(d)(2), Example 1")

-10(d)(3), Example 2")

-10(d)(4), Example 3")

Regulations")

– Proposed Regulations for")

– Proposed Regulations for")

– Proposed Regulations for")

")

")

")

")

")

")